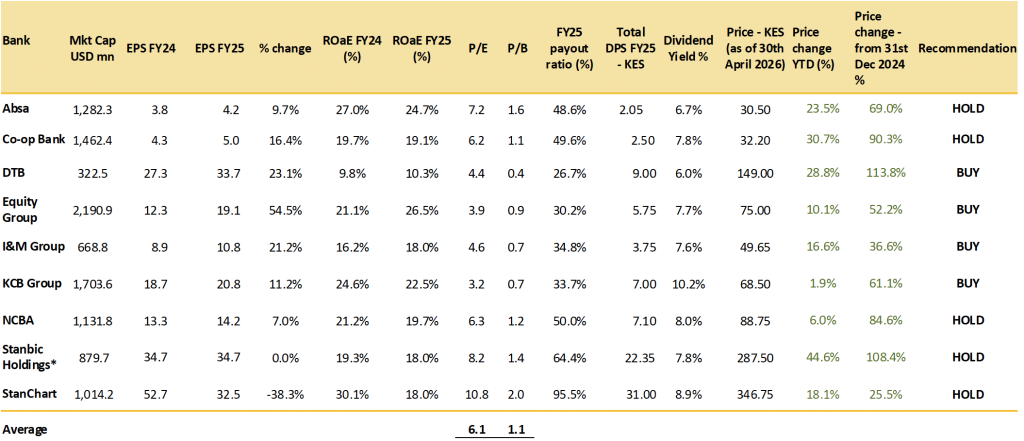

Review of Banking Sector Multiples

Data as at 30th April 2026

USD KES rate at KES 129.19

Source: NSE, Company filings, SIB Estimates, Bloomberg

Definitions:

- ROE: Measures how efficiently a company is generating income from the equity investments of its shareholders; >10% is considered healthy; the higher the better;

- EPS: Measure of a company’s profitability that indicates how much profit each outstanding share of common stock has earned; the higher the better.

- Dividend yield: Represents the dividend amount a company pays annually compared to its share price.

- Payout ratio: Calculated by dividing the total dividends by the total net income of a company.

- P/E: The price an investor is willing to pay for each shilling of a company’s earnings.

- P/B: Calculated by dividing a company’s market price by its book value of equity (shareholders’ equity per share). A ratio below one indicates that a company is undervalued, while a ratio above one indicates that the company’s stock is trading at a premium.

Stock Recommendations Summary

| Absa | •For FY26, management opines that lending rates appear to have bottomed out, and they do not see a significant drop in rates compared to those witnessed in 2025 following successive CBR rate cuts. As such, NIMs are expected to remain largely stable, with potentially higher loan volumes in the coming quarters, spurred by its expansion in the branch network and the implementation of the revised loan pricing model. •Overall, the lender has recorded a laudable performance despite falling margins as it leverages differentiated revenue streams and lower provisions to support earnings. •Absa’s ambitions to scale its new businesses, expand its physical (yet to have presence in 10 counties) and digital distribution channels, partner with strategic providers, and leverage its ecosystem prepositions are still on track. •Potential of increased competition on its Corporate and Investment Banking business from NedBank through the planned acquisition of NCBA Group. | Updated Fair Value Estimate: KES 32.84 Recommendation: HOLD FY25 earnings commentary here |

| Co-op Bank | •The lender has a target of reaching KES 1.0tn in total assets by aggressively deepening its dominance in Kenya and the region; recently announced intention to create a holding company structure which may offer a scalable platform for expansion. •Strong capital and liquidity base to offer headroom to lend, coupled with a sustainable revenue growth trajectory, captive ecosystems, and stable dividend policy. •Lower interest rates may help address the NPL stock, providing headroom for the unwinding of loan loss provisions and suspended interest. •Potential for improved interest income performance in 2026 on the back of higher volumes, as the Group has demonstrated strong momentum in credit demand in 2025 (should market conditions remain conducive). •Diversified revenue streams are anticipated to support Group earnings in the long term. Costs are, however, expected to remain elevated in the near term as it continues to implement expansion and digitization initiatives. | Updated Fair Value Estimate: KES 34.64 Recommendation: HOLD FY25 earnings commentary here |

| Diamond Trust Bank | •The Group continues to leverage its business strategy to grow both conventional and digital customer numbers through accelerated digital transformation coupled with telco partnerships, expanded branch network, and scaling of ecosystem banking in its target key sectors. •As the Group makes headway in asset quality improvement, management has reported that it is targeting a single-digit NPL ratio by the end of FY26, as it leverages reinforced credit underwriting & monitoring, as well as recovery mechanisms. •Group’s cost-to-income ratio to remain elevated in the near term as it implements its DTB 3.0 strategic plan. •The Group’s ROE underperforms the sector by a wide margin, though we see opportunities for improvement in the coming years as it continues to implement its strategic plan. •Discounted P/B ratio, consistent revenue & dividend growth, and expansion efforts provide much-needed confidence in the stock as a long-term play. | Updated Fair Value Estimate: KES 259.97 Recommendation: BUY FY25 earnings commentary here |

| Equity Group | •We see the diversification of revenue streams and the Group’s regional footprint as a tailwind to Group earnings, as it leverages its extensive branch network, payment systems, and tech capabilities to cross-sell its bundled solutions, as well as the robust economic momentum in its operating markets such as DRC, Rwanda, and Tanzania. The Group is reportedly looking into Angola, Zambia and Mozambique as potential market entries. •Equity Group’s Insurance business is tracking well, propelled by its life, general, and health underwriting licenses, with gross written premiums jumping by 75% y/y to KES 9.2bn (PBT up 36% y/y to KES 2.0bn, and a 150% y/y rise in insurance revenue to KES 3.4bn. •Ample liquidity (liquidity ratio up to 64.7% from 57.4% in FY24) provides the Group with headroom to lend to clients across the Group as credit demand momentum picks up. •Management sees the reduction in the Group’s NPL ratio to between 7.0% to 9.0% in 2026 through the resolution of pending bills, court litigation, and recoveries (NPLs appear to have peaked in 1Q25). Risks to the outlook remain, such as the potential economic impact of the US-Iran war, flare-up of hostilities in Eastern DRC, etc. | Updated Fair Value Estimate: KES 114.89 Recommendation: BUY FY25 earnings commentary here |

| I&M Group | •The Group’s outlook remains positive (subject to market conditions) as private sector lending gradually picks up on easing interest rates, with management projecting an ambitious loan book growth rate of c.12.0% – c.18.0% in 2026. •I&M’s target segments are expected to continue supporting revenue performance via growing customer numbers, strategic partnerships, ecosystem focus, and growth of its non-banking subsidiaries. •The lender’s bancassurance and asset management businesses (looking to expand in the regions) are progressing well, with AUM up 2.2x y/y to KES 99.0bn and 68% y/y growth in bancassurance premiums. •As the Group enters the final year of its Imara 3.0 strategy, operating expenses are expected to remain elevated in the near term as the lender grows its branch presence and invests in digital capabilities. •I&M Bank has launched a new Medium-Term Note (MTN) programme of up to KES 20 billion, with Tranche 1 aiming to raise KES 10 billion, plus a KES 3 billion greenshoe option, aimed at supporting onward lending and strengthening Tier II capital. •Risks to the outlook remain, driven by ongoing geopolitical developments and regulatory changes, as well as their potential impact in the markets in which the Group operates. | Updated Fair Value Estimate: KES 65.30 Recommendation: BUY FY25 earnings commentary here |

| KCB Group | •While pressure on asset yield margins remains, we anticipate the Group’s NIM to benefit from lower interest expenses, as it reprices expensive deposits as loan volumes grow. •Management sees a gradual decline in gross NPLs in the coming quarters through the continued payment of pending bills, enhanced recovery initiatives, full and final settlements, and rehabilitations. •Though non-funded income (NFI) eased in the year, we anticipate that growing customer numbers, rising digital loans, enhanced channel optimization, and the acquisition of strategic payments providers (Pesapal, Riverbank – acquired at KES 1.4bn for 75% stake) will serve as a tailwind to NFI in the near term. •With regards to inorganic growth, the Group is currently conducting a deep market assessment of Ethiopia to assess the business case of market entry. We acknowledge the risks associated with the potential impact of a prolonged US-Iran war, the ongoing closure of branches in Eastern DRC, and the translation impact on Group earnings. •The KES 4.00 special dividend paid in FY25 following the sale of NBK is considered a one-off. KCB Group booked a gain of KES 2.7bn net of tax from the sale of NBK. | Updated Fair Value Estimate: KES 96.35 Recommendation: BUY FY25 earnings commentary here |

| NCBA | •Following the completion of the acquisition transaction (3Q26 subject to regulatory approvals), NCBA will become a subsidiary of Nedbank; the entry of Nedbank will bring with it a robust capital base, advanced cross-border infrastructure, access to global markets, and expertise in corporate and investment banking as it supports NCBA’s digital ecosystem, enhances customer propositions, and accelerates its East African market positioning. The offer opens on 28th May 2026, with the closure date slated for 10th July 2026. •Gradual recovery in loan volumes anticipated as demand for private sector credit ticks up (should market conditions remain stable) and as banks in the industry implement their revised risk-based pricing models. •NCBA’s non-banking subsidiaries and digital banking businesses are performing well, with strong wealth management acquisition, growth in bancassurance premiums, and scaling of digital lending capabilities through strategic partnerships. •We view the bank as an income stock given its sustained dividend payments (4-year average dividend payout ratio of c.44.1%), long-term play for those who will opt to retain their stake in NCBA as the Group transitions to a new strategic cycle. | Updated Fair Value Estimate: KES 91.43 Recommendation: HOLD FY25 earnings commentary here |

| Stanbic Bank | •Stanbic’s FY25 performance reflected the normalization of income performance, dampened by the impact of the c.225bps CBR cuts in the year, as well as stable currency movements. We see potential for long-term growth in non-interest revenue due to diversification of revenue streams and pick up in NII as private credit picks up. Assets under custody increased by 34% y/y, reaching KES 824bn, while AUM grew by 1.1x y/y to KES 5.2bn. •The Group aims to continue leveraging opportunities from affordable housing financing, ongoing privatization opportunities, private-public partnerships, G2G oil importation support, and liability management proposition, amongst others. •The lender’s strategic imperative is to achieve a 60% dividend payout (dependent on sufficient capital thresholds). | Updated Fair Value Estimate: KES 280.73 Recommendation: HOLD FY25 earnings commentary here |

| Stanchart | •The lender’s FY25 performance indicated a normalization of revenue as margins narrowed, further constrained by a significant one-time staff expense with earnings likely to normalize in 2026. •We view the lender’s commendable asset quality, cross-border network services, diversified investment options, Affluent Business pivot, access to capital pools (e.g., USD 100m risk participation program with BII), digital and sustainability (earned KES 3.5bn in FY25) proposition, and its global presence as key tailwinds to the Group’s revenue performance in the long term. •The lender recorded an impressive uptick in assets under management at KES 302Bn (+29%), partly driven by a consumer shift from fixed deposits and record high Net New Money (+171%), with assets under custody (both international and local) surging to KES 1.7tn (+32%) –driven by higher securities values as well as new business, providing a stable base for fee income. •Furthermore, the low-cost deposit base amid easing interest rates (StanChart fully transmitted the CBR cut benefit to its clients) may help StanChart support its net interest margins as the operating environment shifts. •StanChart remains a dividend play, given its attractive dividend payment policy, provided that it meets its capital adequacy requirements (5-year average of payout of c.81.8%) as the lender continues to implement strategic initiatives to rebuild its profit base following the deterioration experienced in 2025. | Updated Fair Value Estimate: KES 337.39 Recommendation: HOLD FY25 earnings commentary here |