The Year of the Synchronized Pivot

Warren Buffett loves to quote his mentor Ben Graham, who once said: “In the short run, the market is a voting machine but in the long run it is a weighing machine.” The recently retired Oracle of Omaha often talked about how the stock market resembled a person with “incurable emotional problems,” going back and forth from euphoria to depression. He has talked about buying his first stock in Despite financial panics, costly wars, and high inflation, the market still rose.

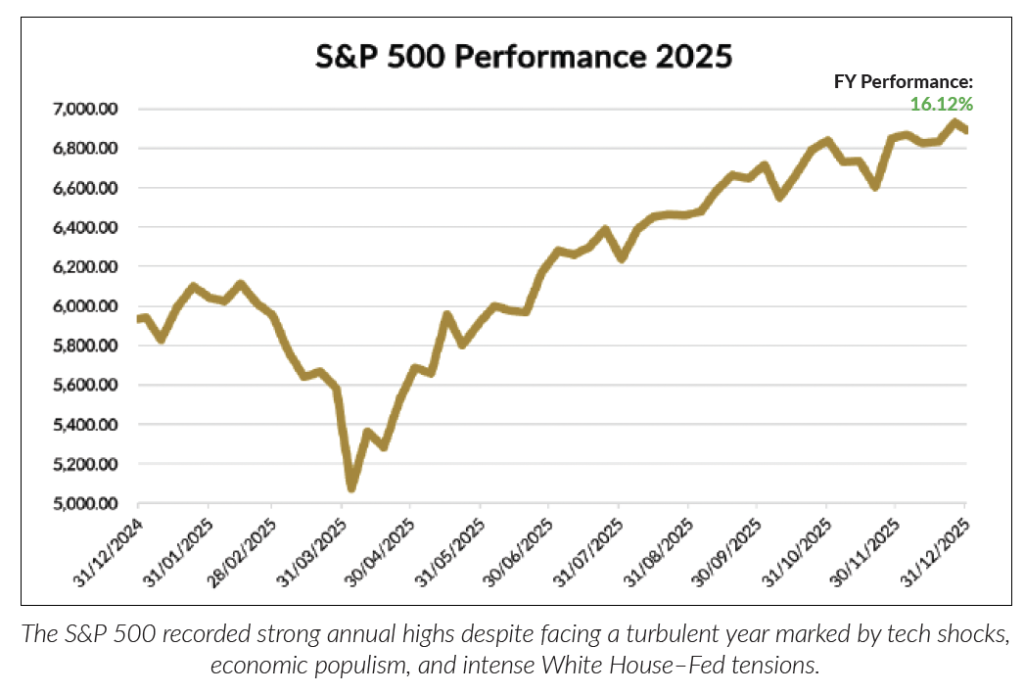

The lesson, he often said, was to filter out macro events, short-term headlines, and stock price volatility, focusing on the underlying fundamentals of a business. “The market may ignore business success for a while, but eventually will confirm it,” he said. Buffett’s lessons and parables remind us of the volatility in stocks over the last year. While the S&P 500 gained over 16% for the year & the tech-laden Nasdaq Composite index posted another 20% year, the road to get there was anything but smooth with the U.S. equity market being repeatedly stress-tested by technological shocks, populist economic experiments, and an unprecedented war of wills between the White House and the Federal Reserve.

The year began with a technological earthquake that fundamentally challenged the thesis powering the bull market. In late January 2025, Chinese startup DeepSeek released its “R1” artificial intelligence model claiming to have achieved performance comparable to leading U.S. models at a fraction of the training cost, utilizing fewer and older chips, a development that sent shockwaves through Silicon Valley and Wall Street. This revelation triggered an existential crisis for the “AI capex” trade, sparking fears that the billions of dollars being poured into Nvidia hardware by U.S. hyperscalers were excessive and that AI efficiency would deflate chip demand. The market reaction was visceral: on January 27, Nvidia shares plummeted 17%, wiping out nearly $600 billion in market value in a single session—the largest one-day loss for any company in history. The “DeepSeek Shock” dragged the entire tech sector lower, as investors grappled with the terrifying prospect that the artificial intelligence boom was a bubble susceptible to commoditization from low-cost overseas competitors.

Just as the market began to stabilize from the tech sell-off, realizing that inference demand would still require massive compute power, volatility struck from a different direction: the White House. On April 2, 2025, in a move characterized as “Liberation Day,” President Trump announced a sweeping regime of tariffs targeting nearly all U.S. imports to address trade deficits. The announcement roiled markets, causing a sharp 19% correction dubbed the “2025 Stock Market Crash” as algorithms and analysts scrambled to price in higher input costs and the risk of global retaliation. The S&P 500 slid aggressively, erasing early-year gains and invoking fears of 1970s-style stagflation. However, the administration, sensitive to the equity market’s performance as a barometer of success, quickly pivoted. By April 9, the White House signalled a pause and a scaling back of the most aggressive levies, triggering a massive relief rally that effectively marked the market bottom for the year. This “TACO” dynamic (Trump Always Chickens Out)— where aggressive trade threats are walked back to preserve market stability—became a recurring theme that traders began to exploit.

As the Trump administration showed a willingness to negotiate trade deals, the narrative shifted from fear to fiscal euphoria with the passage of the “One Big Beautiful Bill Act” (OBBBA), signed into law on July 4, 2025. This legislative juggernaut acted as a potent shot of adrenaline for the U.S. consumer and corporate sector. The bill made permanent the corporate tax cuts from 2017 and introduced a suite of populist deductions that injected liquidity directly into household balance sheets, including “No Tax on Tips,” “No Tax on Overtime,” and deductibility for car loan interest. The economic impact was immediate: consumer spending accelerated in the third quarter, driving GDP growth to an annualized rate of 4.3%. The OBBBA effectively engineered a “soft landing” by subsidizing consumption just as the labor market began to show signs of

fraying, creating a bridge over the economic slowdown that many had feared was inevitable.

However, this fiscal stimulus set the stage for a dramatic institutional clash in the second half of the year. The Federal Reserve found itself caught between a cooling labor market, which required rate cuts, and the inflationary potential of the OBBBA & tariffs. This tension was exacerbated by President Trump’s unprecedented public campaign to force the central

bank’s hand. The hostility peaked in August when the President attempted to fire Federal Reserve Governor Lisa Cook, alleging mortgage fraud in a maneuver widely interpreted as a test case for removing Chairman Jerome Powell. Although the courts intervened to block the firing, the episode injected a risk premium into U.S. assets, raising concerns about the erosion of central bank independence. Despite the political heat and being called a “fool” by the President over renovation costs, Chairman Powell and the FOMC proceeded with a data-dependent pivot. Acknowledging a rise in unemployment to 4.6%, the Fed delivered three consecutive 25-basis-point cuts in September, October, and December, lowering the federal funds rate to a range of 3.50%–3.75%. This monetary easing, delivered despite the fiscal stimulus, provided the final tailwind needed to push equities toward record highs by year-end.

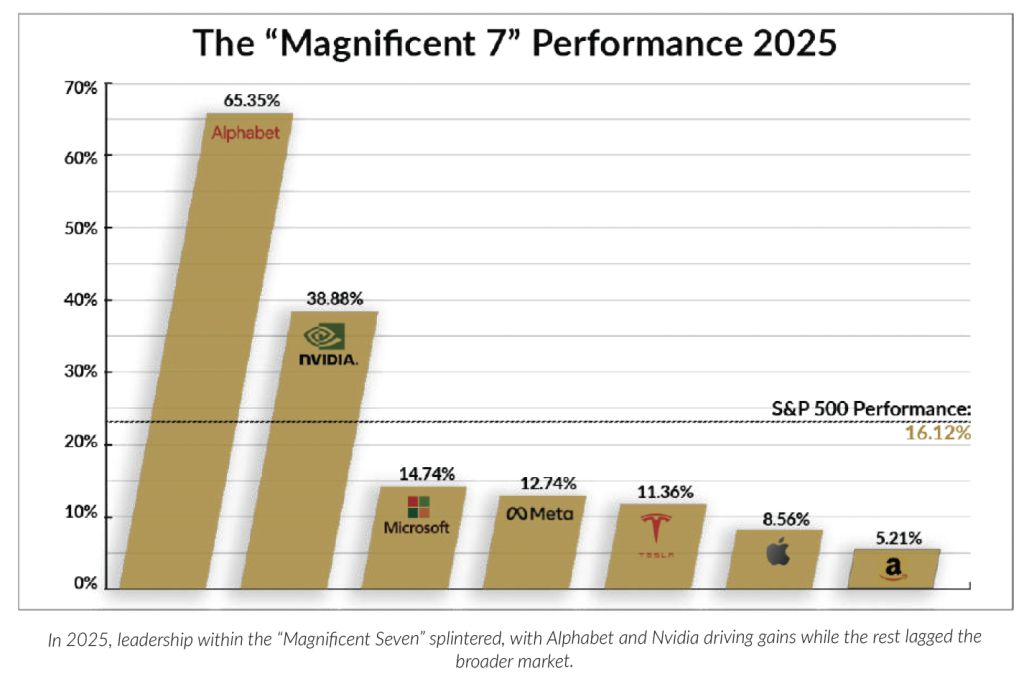

Underneath the surface of the headline indices, the monolithic dominance of the “Magnificent Seven” began to fracture in 2025, giving way to a more complex market leadership. While the group as a whole posted strong returns, the dispersion

was stark. Alphabet emerged as the undisputed champion, surging nearly 66% as its Gemini models reassured investors of its AI competitiveness and cloud revenue continued its acceleration higher. Nvidia, despite the DeepSeek scare, managed to claw back losses and finish up roughly 39%, supported by the reality that data center build-outs were far from over.

Conversely, the remaining members of the magnificent Seven contingent all trailed the broader market for much of the year. The market however, found new darlings outside of the traditional mega-caps, particularly in the “AI infrastructure” trade.