MACRO-ECONOMIC INDICATORS

- Kenyan Shilling Soars: 18.7% Surge q/q, 0.4% y/y against the dollar in 1Q24 – a first quarter fueled by sentiment and behavioral economics

- Secondary bond market sizzles: Turnover skyrockets to KES 459.30bn in 1Q24, up from KES 142.72bn in 4Q23

- Kenyan Eurobond yields dip, normalizing risk pricing post buyback

- In 1Q24, the government recorded a net domestic borrowing of KES 197.68bn, having borrowed KES 730.21bn and redeemed KES 532.53bn

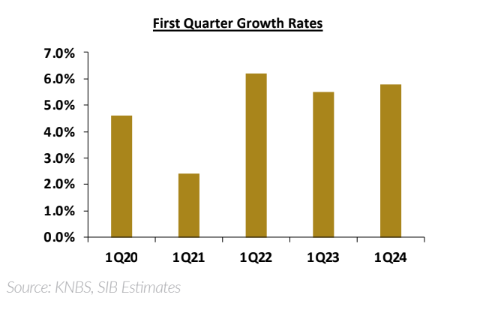

GDP Growth

The Kenyan economy is estimated to have grown by 5.8% in 1Q24, 30bps higher than the 5.5% growth recorded in 1Q23, as shown below:

The growth will be driven by;

- A resilient services sector set to expand by 6.8% compared to 6.2% in 1Q23. The growth is projected to have been supported by robust growth in the financial services and insurance, transport, as well as wholesale and retail trade sectors,

- A strong recovery in agriculture amidst a relatively favourable weather condition, and,

- A Rebound in the industry sector supported by continued recovery in the manufacturing sector.

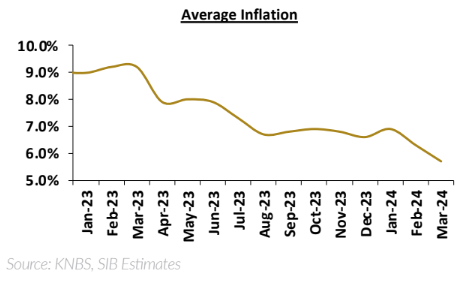

Inflation

The average y/y inflation for 1Q24 stood at 6.3%, 50bps and 280bps lower than the 6.8% and 9.1% average rate recorded in 4Q23 and 1Q23, as shown below;

The slower growth in the general price levels was largely due to the decelaration in both food & fuel inflation which led to a slow down in the food and transport indices as shown below;

| INDEX | WEIGHT | 1Q23 | 1Q24 |

| Food & non-alcoholic Beverages | 32.9% | 13.2% | 6.9% |

| Housing & other Utilities | 14.6% | 7.5% | 8.7% |

| Transport | 9.6% | 13.0% | 10.7% |

The housing and other utilities index remained sticky on a faster growth in electricity prices, both small scale and industrial.

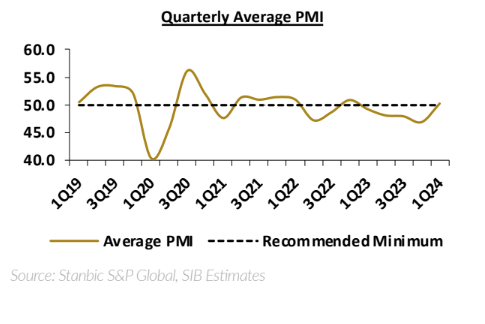

Purchasing Manager’s Index (PMI)

In 1Q24, the private sector business environment exhibited slight expansion with the Stanbic PMI slightly surpassing the 50 mark to an average of 50.3 from 46.9 and 49.3 in 4Q23 and 1Q23, respectively.

The improvement was largely on the back of the reduced inflationary pressures during the quarter which translated to lower input costs and overall improvement in demand. See the chart below;

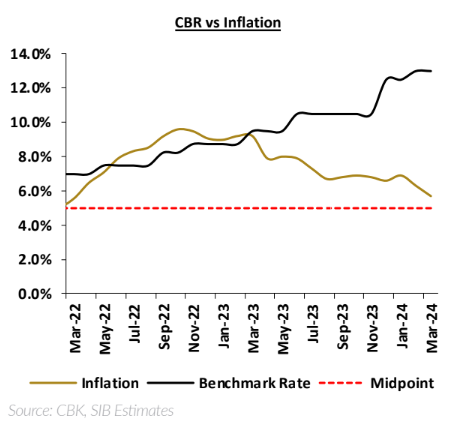

Central Bank Rate (CBR)

The Monetary Policy Committee met once during the quarter and raised the CBR by 50bps to 13.0% citing the need to anchor inflation towards the midpoint of the target range; (2.5% – 7.5%). See below the movement of the rate over the years;

We opine that 1Q24 may be the boarderline from which we are unlikely to see major rate hikes going forward.

Inflation is rapidly approaching the midpoint and the shilling continues to strengthen against the dollar, hence supporting price stability.

Currency

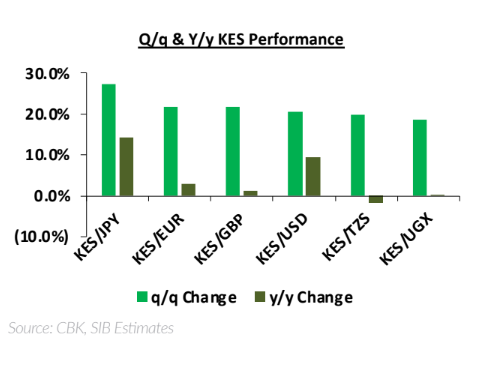

In 1Q24, the Kenyan shilling recorded an 18.7% q/q and 0.4% y/y gain against the dollar. The steep appreciation in over a decade during the first quarter was mainly a behavioral economics and sentiment play supported by;

- The 2024 Eurobond buyback,

- Excellent performance of the new Eurobond issuance and the February infrastructure bond,

- Panic selling of dollars on uncertainty of the shillings equilibrium point.

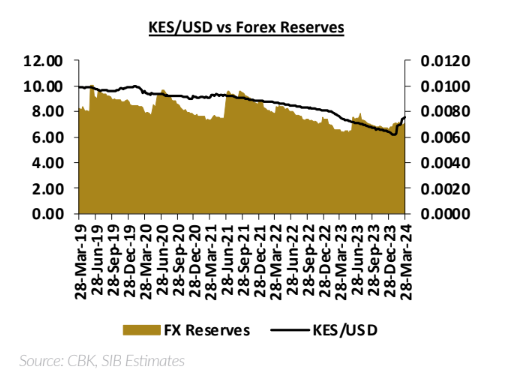

Kenya’s forex reserves ended 1Q24 on a higher note but remained below the statutory requirement of four months of import cover (MIC). The reserves stood at USD 7.09bn (3.8 MIC), a 7.2%q/q and 8.2% y/y increase. The increase was largely on external financing as well and possible interventions from the foreign exchange market. See below a chart showing the performance of the shilling vs FX reserves;

The shilling appreciated against all major relevant currencies. See below a summary of the performance;

Diaspora Remittances

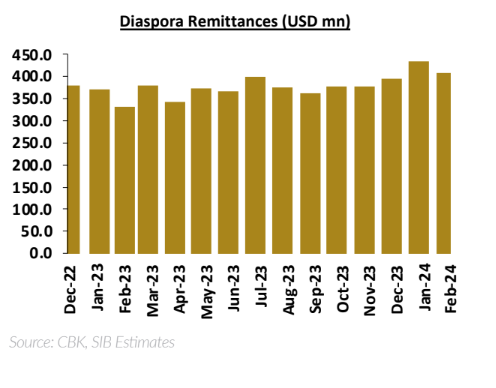

As of February 2024, the cumulative diaspora remittances over the last quarter stood at USD 1.17bn, a 15.3% increase from USD 1.03bn recorded over the same period in 2023. See below the chart;

Kenya’s Domestic Debt

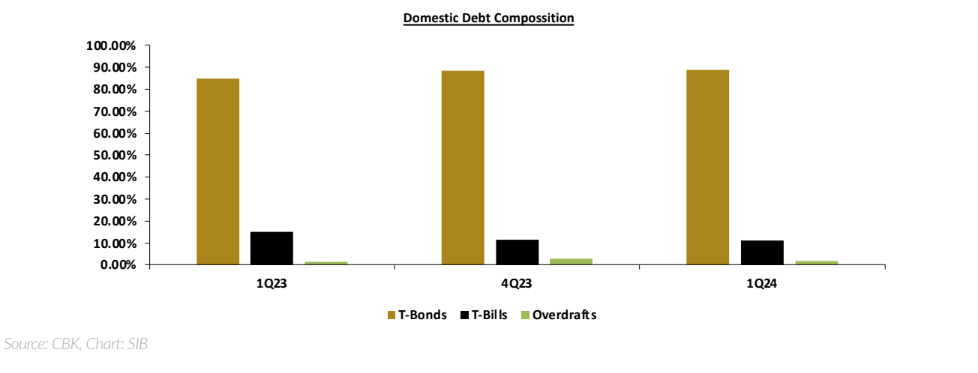

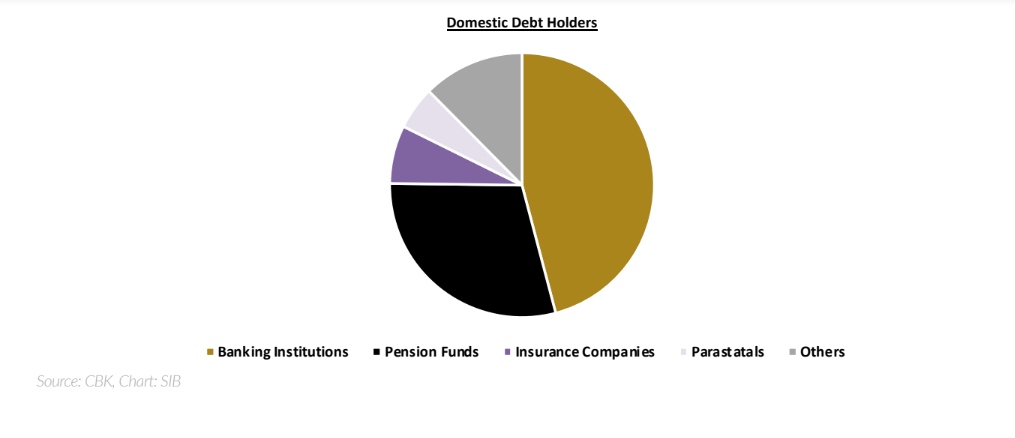

As of 22nd March 2024, treasury bonds accounted for 88.9% of Kenya’s domestic debt. The country’s domestic debt stock increased by 3.6% q/q and 15.2% y/y to KES 5.23tn, from KES 5.05tn and KES 4.54tn. In 1Q24, the government recorded a net domestic borrowing of KES 197.68bn, having borrowed KES 730.21bn and redeemed KES 532.53bn. See below a summary of Kenya’s domestic debt;

Banking institutions remain the largest holders government’s domestic debt holding 45.89% as of 22nd March 2024. Pension funds follow accounting for 29.3%, 620.0bps lower than the amount held at the end of 2023. See below the country’s domestic debt by holder;

FIXED INCOME MARKET

Performance

T-Bills

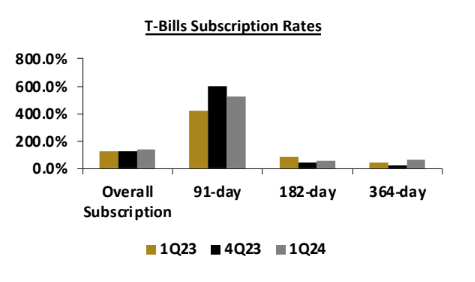

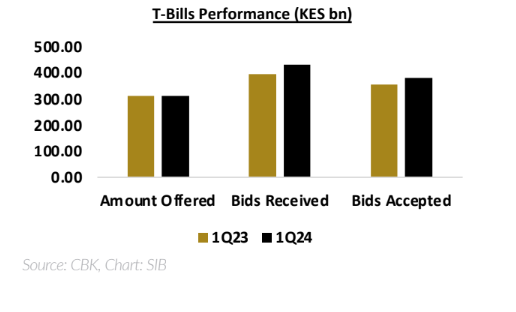

In 1Q24, Treasury bills were oversubscribed with the average subscription rate coming in at 137.8%, up from 128.6% recorded in 4Q23. Demand for the 91-day paper persisted, recording an overall performance rate of 522.1%, down from 602.7%, in the previous quarter. The overall subscription was weighed down by sub par performance of the 182-day and 364-day papers which recorded a subscription rate of 58.5% and 63.3%, respectively.

Out of the KES 429.86bn worth of bids received, KES 382.10bn was accepted translating to an acceptance rate of 88.9%. See below a summary of the performance;

T-Bonds

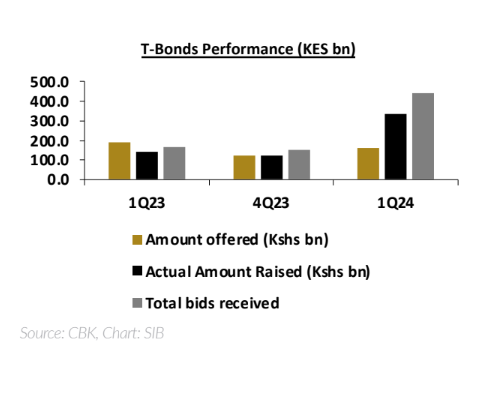

Treasury bonds were also oversubscribed with the overall subscription coming in at 275.3%, up from 121.5% in 4Q23. The Central Bank of Kenya reopened and issued two new bonds. Investors interest leaned mostly towards the February infrastructure bond which accounted for 65% of the total bids received during the quarter.

Overall, the government raised KES 334.61bn, translating to a 75.9% acceptance rate. See below a summary of the performance;

Secondary Bond Market

The secondary bond market turnover more than quadrupled to KES 459.30bn in 1Q24, from KES 142.72bn in 4Q23. The q/q increase was mainly on account of significant trades on the February infrastructure bond which fetched the highest tax free coupon (18.5%) at the NSE in recent memory. See below a summary of the performance;

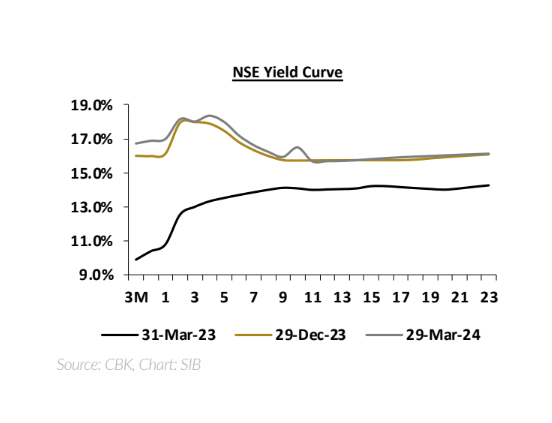

Yields

The yield curve remained inverted in 1Q24 with the yields on government papers increasing by a cumulative 711.5bps q/q.

Short term papers climbed by a cumulative 281.8bps, while medium term papers rose by 301.7bps and the long term papers by 128.1bps. See below the yield curve;

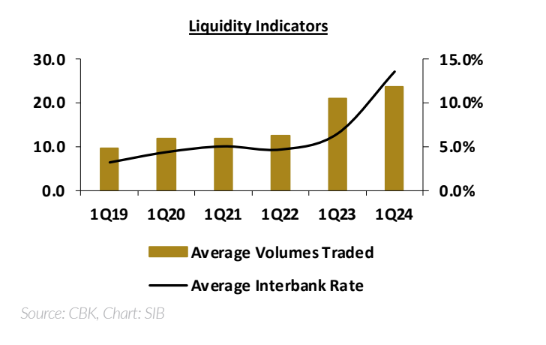

Money Market Liquidity

Liquidity in the money market remained constrained during the quarter with the average interbank rate jumping 183.2bps and 712.2bps to 13.6%, from 11.8% and 6.5% in 4Q23 and 1Q23, respectively.

The jump was mainly attributable to the requirement that the interbank rate tracks the Central Bank Rate which was raised a cumulative 375bps in 2023 and 50bps in

1Q24. See the chart below;

However, the Central Bank maintained its support to liquidity strapped entities having injected more than KES 1.97tn during the quarter, 48.1% higher than the KES 1.33tn injected in 4Q23.

Kenyan Eurobonds

Yields on all Kenyan Eurobonds declined and adjusted to a normal curve suggesting appropriately priced risks. The decline was largely influenced by the Eurobond buyback.

In addition, the National Treasury issued a new Eurobond; KENINT 2031 whose proceeds were used to buyback the June Eurobond. KENINT 2031, has an outstanding principal of USD 1.5bn, a 9.75% coupon rate and an amortized maturity structure, meant to lower the overall costs associated with the bond. See below a summary of the performance;

Disclosure and Disclaimer

Analyst Certification Disclosure: The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed and attributed to the research analyst or analysts in the research report accurately reflect their personal opinion(s) about the subject securities and issuers and/or other subject matter as appropriate; and, (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report.

Global Disclaimer: Standard Investment Bank (SIB) and/or its affiliates makes no representation or warranty of any kind, express, implied or statutory regarding this document or any information contained or referred to in the document. The information in this document is provided for informational purposes only. It does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices, or represent that any such future movements will not exceed those shown in any illustration. The stated price of the securities mentioned herein, if any, is as of the date indicated and is not any representation that any transaction can be effected at this price. While reasonable care has been taken in preparing this document, no responsibility or liability is accepted for errors of fact or for any opinion expressed herein. The contents of this document may not be suitable for all investors, as it has not been prepared with regard to the specific investment objectives or financial situation of any particular person. Any investments discussed may not be suitable for all investors. Users of this document should seek professional advice regarding the appropriateness of investing in any securities, financial instruments, or investment strategies referred to in this document and should understand that statements regarding future prospects may not be realised. Opinions, forecasts, assumptions, estimates, derived valuations, projections, and price target(s), if any, contained in this document are as of the date indicated and are subject to change at any time without prior notice. Our recommendations are under constant review. The value and income of any of the securities or financial instruments mentioned in this document can fall as well as rise, and an investor may get back less than invested. Future returns are not guaranteed, and a loss of original capital may be incurred. Foreign-currency denominated securities and financial instruments are subject to fluctuations in exchange rates that could have a positive or adverse effect on the value, price, or income of such securities and financial instruments. Past performance is not indicative of comparable future results, and no representation or warranty is made regarding future performance. While we endeavour to update on a reasonable basis the information and opinions contained herein, there may be regulatory, compliance, or other reasons that prevent us from doing so. Accordingly, information may be available to us which is not reflected in this material, and we may have acted upon or used the information prior to or immediately following its publication. SIB is not a legal or tax adviser and is not purporting to provide legal or tax advice. Independent legal and/or tax advice should be sought for any queries relating to the legal or tax implications of any investment. SIB and/or its affiliates may have a position in any of the securities, instruments, or currencies mentioned in this document. SIB has in place policies and procedures and physical information walls between its Research Department and differing business functions to help ensure confidential information, including ‘inside’ information, is not disclosed unless in line with its policies and procedures and the rules of its regulators. Data, opinions, and other information appearing herein may have been obtained from public sources. SIB makes no representation or warranty as to the accuracy or completeness of such information obtained from public sources. You are advised to make your own independent judgment (with the advice of your professional advisers as necessary) with respect to any matter contained herein and not rely on this document as the basis for making any trading, hedging, or investment decision. SIB accepts no liability and will not be liable for any loss or damage arising directly or indirectly (including special, incidental, consequential, punitive, or exemplary damages) from the use of this document, howsoever arising, and including any loss, damage, or expense arising from, but not limited to, any defect, error, imperfection, fault, mistake, or inaccuracy with this document, its contents, or associated services, or due to any unavailability of the document or any part thereof or any contents or associated services. This material is for the use of intended recipients only, and in any jurisdiction in which distribution to private/retail customers would require registration or licensing of the distributor, which the distributor does not currently have, this document is intended solely for distribution to professional and institutional investors.