Turbulence, tariffs and the tech unwind

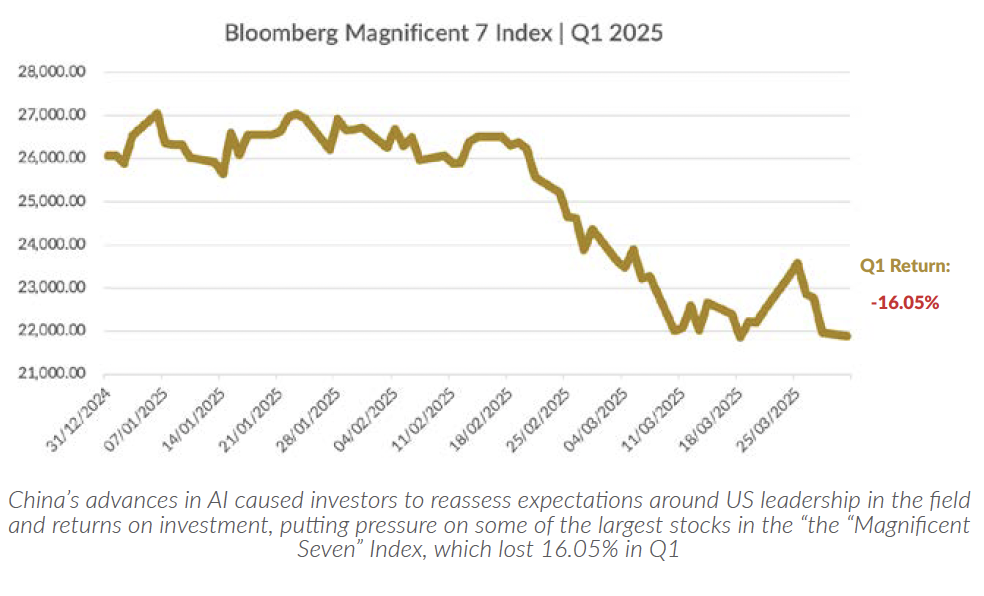

Stocks went into the start of 2025 with the bull market solidly intact, albeit with valuations beginning to look stretched. The Fed appeared to have achieved a soft landing for the economy, and investors were still looking forward to rate cuts. That backdrop began to change as news that China’s DeepSeek had developed an artificial intelligence (AI) model comparable to market leaders, but at a fraction of the cost, caused investors to reassess expectations around AI, US leadership in the field, and returns on investment. Specialists said DeepSeek’s technology still trails that of OpenAI and Google. But it is a close rival despite using fewer and less-advanced chips, and in some cases skipping steps that U.S. developers considered essential. The AI theme has powered stock markets in recent years, contributing to the outperformance of the “Magnificent Seven” group of stocks, and so the news put pressure on some of the largest stocks in the index with this contingent collectively losing over 16% during this quarter.

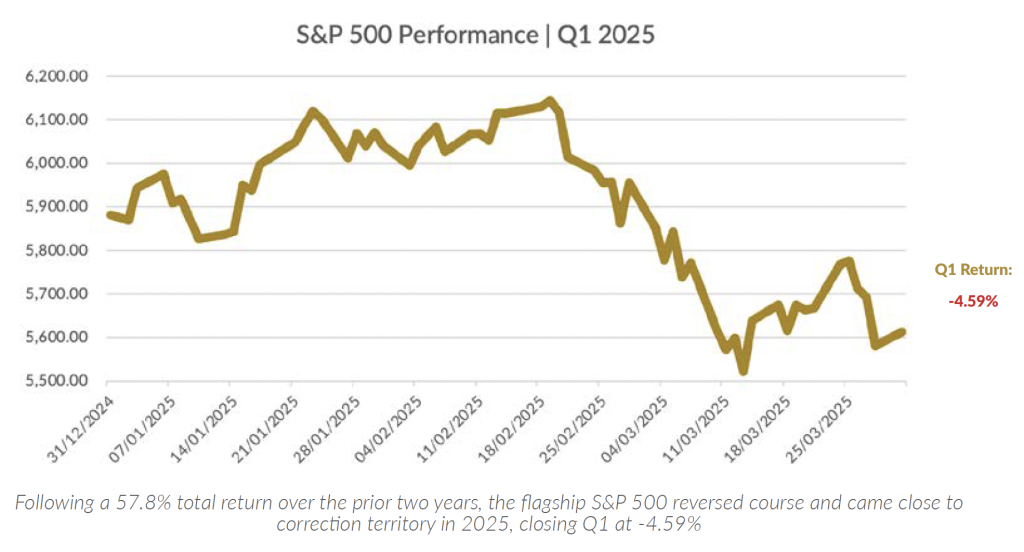

Following a 57.8% total return over the prior two years, marking its best two-year performance since 1998 (26 years), the flagship S&P 500 reversed course and came close to correction territory in the new year. Fear of consequences from potential policy changes drove the S&P 500’s dramatic decline of over 10% between February 19 and March 13, one of the fastest market corrections in the past century, leading to its worst quarterly performance (-4.6%) since the peak of the hiking cycle in Q3 2022. Typically, a rapid correction more closely follows fundamental triggers like surprising economic reports, a banking crisis, or government defaults.

This time, however, the sharp sell-off stemmed primarily from mounting investor anxiety around the aggressive and haphazard nature of the undertakings by the newly formed Department of Government Efficiency (DOGE), led by Elon Musk as a “special government employee,” and potential trade policies proposed by the Trump administration. As policy uncertainty spiked to levels not seen since the pandemic, business and consumer confidence deteriorated and weighed on investor sentiment.

As policy uncertainty spiked to levels not seen since the pandemic, business and consumer confidence deteriorated and weighed on investor sentiment.

Aside from the Nasdaq-100, which benefitted in December with greater weightings towards large-cap growth, the major equity indices (S&P 500, Dow Jones Industrial, S&P Mid-Cap 400 & Russell 2000) registered monthly declines in three of the prior four months starting in December. Large-cap growth held up near its cycle highs into mid-February before succumbing to the rotation of selling pressure. From a glass half full perspective, most large-cap sectors experienced their greatest declines in December and downside momentum has since been waning with eight of the 11 sectors having a positive Q1.

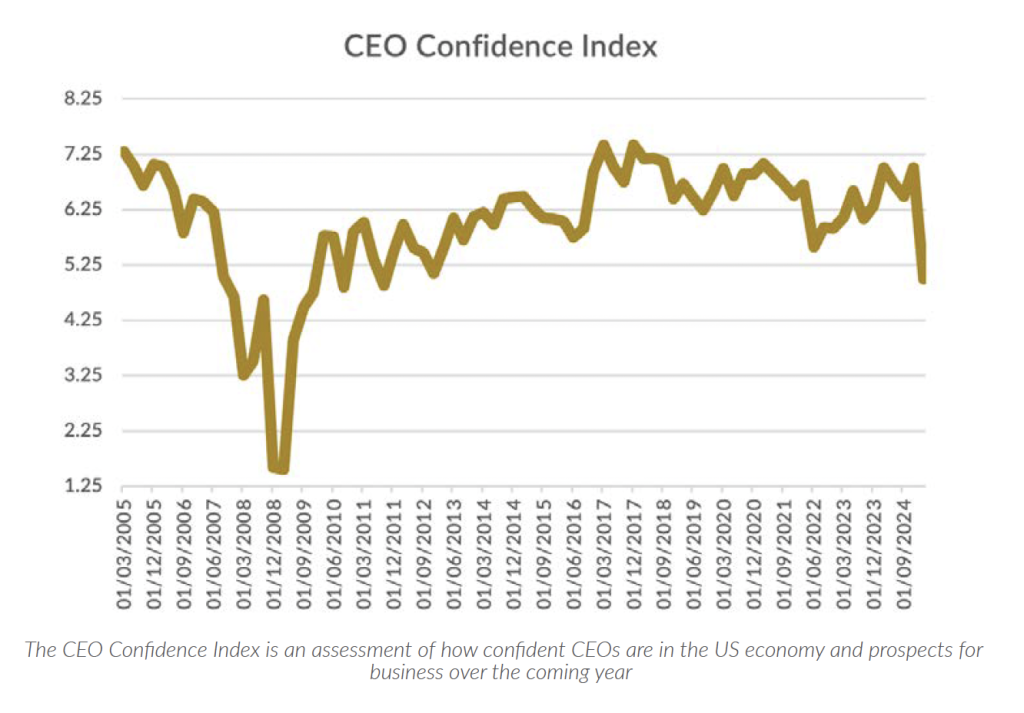

Trade tariffs increasingly became a key theme towards the end of the quarter as President Trump announced tariffs on certain countries (notably Mexico and Canada) and on some goods (cars, steel, aluminium). Meanwhile, U.S. economic data throughout the quarter showed signs of an economy that is cooling. Housing inventories have risen to pre-covid levels raising concerns there could be a slowdown in residential construction later this year. The 30-year fixed-rate mortgage fell to 6.65% in late March, but it likely needs to move lower to improve existing home sales which for two years have been hovering at levels last seen during covid and the GFC eras. While employment appears solid, there are signs amidst quit rates, real wages, new hires, and average weekly hours which may suggest future upward pressure in the unemployment rate. Consensus at the start of the year projected 2025 Real GDP of 2% for the US, however the widely referenced Atlanta Fed GDPNow economic model now projects a substantial contraction (-2.8%). The uncertainty brought about by the DOGE efforts and Trump’s trade policy has resulted in the CEO confidence index plummeting to levels last seen back in 2010. The CEO confidence index is a barometer of the health of the US economy from the perspective of US chief executives. The measure is based on CEOs’ perceptions of current and expected business and industry conditions gauging expectations about future actions their companies plan on taking in four key areas: capital spending, employment, recruiting, and wages over the next 1 year.

Amidst this, The Federal Reserve paused its rate cutting cycle with Chair Powell affirming the Fed is in “no hurry” to cut rates at the most recent March FOMC. The Fed’s quarterly Summary of Economic Projections revised growth lower (from 2.1% to 1.7% GDP) and higher inflation (core-PCE from 2.5% to 2.8%) for 2025 but held constant its Interest Rate guidance at 3.9%, implying just two 25bp rate cuts. The Fed noted the economy is in good shape but also placed strong emphasis on the increasing uncertainty surrounding the economy and its future projections. Some argue the Fed’s monetary policy is too tight, creating a passive tightening effect by waiting for bad news to act which puts excess strain on cyclical areas of the market. The old market mantra “don’t fight the Fed” has been replaced by “don’t fight the Treasury” highlighting the Trump administration’s focus on the bond market as they are seemingly willing to tolerate pain in the equity markets if it results in Yields on the 10-Year Treasuries keep coming down.