Banks struggle to protect profitability in 2025 as FX and interest incomes fall

Full Report:

Overview:

Listed banks in our coverage for the period 1Q25 exhibited flat overall profitability, weighed down by sluggish credit demand amid struggling interest and FX income.

Notably:

- Industry PBT at KES 73.5bn in 1Q25 (unchanged from 1Q24), largely attributable to a comparatively lower decrease in income compared decrease in expenses.

- Coverage PAT hit KES 64.4bn (-0.6%y/y); however, total interest expenses tapered at a much faster pace (-14.1% y/y) compared to the slowdown in total interest income (-0.9%y/y), supporting the topline.

- Significant decline in FX income (-41.0%y/y to KES 13.0bn) exerted downward pressure on non-funded income as the local unit remains stable.

- A notable 20.3%y/y slash in total loan loss provisions to KES 17.9bn helped to buffer coverage bottom line as lenders priced in potential improvement in asset quality in the coming quarters.

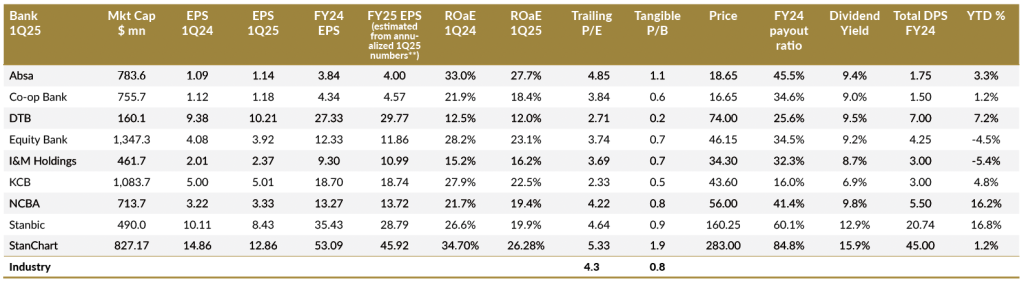

Review of banking sector multiples: Low valuation, long-term potential

Data as at 20th June 2025

** We are currently updating our models and will provide fair value estimates in due course

Source: NSE, Company filings, SIB Estimates, Bloomberg

Definitions:

- ROE: Measures how efficiently a company is generating income from the equity investments of its shareholders; >10% is considered healthy; the higher the better;

- EPS: Measure of a company’s profitability that indicates how much profit each outstanding share of common stock has earned; the higher the better.

- Dividend yield: Represents the dividend amount a company pays annually compared to its share price.

- Payout ratio: Calculated by dividing the total dividends by the total net income of a company.

- P/E: The price an investor is willing to pay for each shilling of a company’s earnings – If below average, considered undervalued.

- P/B: Calculated by dividing a company’s market price by its book value of equity (shareholders’ equity per share). A ratio below one indicates that a

- company is undervalued, while a ratio above one indicates that the company’s stock is trading at a premium.

Stock Recommendation

| Absa | • While Absa’s Cost-to-Income deteriorated to 35.0% from 33.9% in 1Q24, this remains best in class compared to its peers. • We note the normalisation of the Group’s earnings against a higher base in 2024, as interest rates declined and currency volatility eases. Nonetheless, we see NIMs being propped up by lower interest expenses on lower rates as the CBK focuses on encouraging lending to the private sector, which may compensate for the slowdown in interest income. • We believe that the lender’s continued product diversification (e.g. increased focus on wide-ranging financial instruments, e.g. currency swaps, the targeted launch of MSCI-linked ETF in 2Q25). • Growth in NPLs remains a concern; however, its Gross NPL ratio remains below the industry average. • We opine the lender will focus more on short-term working capital lending, secured loans, and target payrolls that pass through the bank as it leverages increased collections and recoveries/tighter credit risk management to manage asset quality. | BUY Full Report here |

| Co-op Bank | • We anticipate that declining interest rates will ease interest expense on liabilities and pressure on asset quality, providing headroom for the unwinding of loan loss provisions. • The lender posted commendable interest income growth on better yields on interest-earning assets. • Furthermore, the Group’s management expects the cost of funds to trend lower (<5.0% in FY25), thereby reducing elevated interest expenses as the Group sheds expensive deposits. • From our vantage point, the lender may position itself to tap into the potential direct integration of Sacco into the National Payment System, banking on its innate expertise in Sacco’s operations. As such, management does not envisage significant disruption should the reforms come into place. • The South Sudanese government and key oil firms announced the resumption of oil production and export, which may act as a tailwind to its South Sudan subsidiary’s revenues. • Strong capital and liquidity base to offer headroom to lend, coupled with a sustainable revenue growth trajectory, captive ecosystems, and stable dividend policy; Co-op recently appeared on the Financial Times list of Africa’s fastest growing firms. | BUY Full Report here |

| Diamond Trust Bank | • We see the lender’s growth initiatives, diversified revenue lines (custody business, agency banking), ecosystem focus and target sectors (education, agriculture, public sector, technology), strategic tech & industry partnerships, digital transformation, coupled with regional subsidiaries as tailwinds to the Group’s long-term outlook. • We laud the lender’s asset quality improvement, with management forecasting NPL improvement in the year, underpinned by recoveries of existing impaired assets. • The bank’s costs are poised to remain elevated as it continues to expand, and are likely to yield long-term efficiency and customer base growth. • Deeply discounted P/B ratio, consistent revenue & dividend growth, and expansion efforts provide much-needed confidence in the stock as a long-term play. | BUY Full Report here |

| Equity Group | • We anticipate continued improvement in EBKL’s performance, propelled by declining interest expenses, a growing loan book and diversification of revenue lines driving NFI. • Notwithstanding the currency impact on regional currencies, the lender’s regional play largely continued to bear fruit, with strong performance recorded by Rwanda, Uganda and Tanzania on a constant currency basis. • Despite the marked slowdown driven by instability, management remains optimistic about Equity BCDC, with ongoing security talks as well as the potential resumption of cobalt exports. • With the lender having activated its general insurance offering in 2025 in Kenya (the Group is in the process of acquiring a health insurance subsidiary license), we see diversification of revenue streams as a tailwind as the Group leverages its wide branch network to cross-sell its bundled solutions. • While asset quality remains a concern, the possible reduction in outstanding NPLs through the potential resolution of pending bills, court litigation, and recoveries is poised to buoy interest income as suspended interest (printed at KES 29.1bn in 1Q25) is released. | BUY Full Report here |

| I&M Group | • The Group reported a commendable performance in 1Q25, considering the tepid industry conditions. • The subscription transaction is projected to pump in additional capital (c. KES 4.2bn), which is anticipated to support the lender’s strategic initiatives going forward, including looking at opportunities in contiguous countries based on business flows. • We continue to see growth in the Group’s Corporate and Institutional Banking segment, buoyed by cross-border business, target sector focus (Oil and Gas, China desk, Leasing, Public Sector), and ecosystem play. • We expect the Personal and Business Banking segment to grow on the back of enhanced propositions: unsecured digital lending, stock financing, digital self-onboarding, etc. • We opine I&M’s target segments will support NFI performance on the back of growing customer numbers, supported by the latest announcement regarding implementation of revised service tariffs effective May 2025 (bank-to-mobile money transfers remain free). | BUY Full Report here |

| KCB Group | • While KCB Group delivered a flat performance in EPS in 1Q25, we find it commendable coming from a high base in 2024. • Group’s NIM to continue benefiting in the short term from lower interest expenses as the year progresses. • Non-performing loans remain a concern, having hit a record high of KES 233.3bn. The anticipated issuance of the Kenya Roads Bond may help reduce its NPL stock. Additionally, the sale of NBK could partially alleviate concerns about asset quality. • Completion of NBK KCB deal points to potential special/interim dividend, depending on capital levels. • Sustained revenue performance backed by strategic partnerships, digital & payments initiatives, revenue diversification, and regional play, coupled with management’s target of subsidiary dividend payments to the Group as regional business picks up (bulk of the Group dividend currently comes from KCB Kenya). | BUY Full Report here |

| NCBA | • The Group posted muted performance in 1Q25, on the back of tighter FX margins, coupled with lower interest income. • While Central Bank Rate cuts should cut interest costs, lending rates are also likely to fall, with overall margins determined by a balancing act. • We expect operating costs to remain elevated in the medium term, given the ongoing digital and physical expansion initiatives, though management notes that the Group is at the inflection of efficiency as of FY24, having reached the peak of its investment cycle (target of CIR of 45%). We note the potential overhang of the High Court’s recent decision to nullify the KES 384.5m tax waiver granted during the 2019 NIC-CBA merger. • Overall, we like the take-off of NCBA IG insurance, the Group’s growing digital loan book, regional play, product & channel diversification and a robust wealth management business, which should help secure solid profitability in the long term. | BUY Full Report here |

| Stanbic Bank | • Tight income performance coming off a high-interest rate environment, with lower CBR rates and stable currency movements. • Growth opportunities for the lender in the medium term from strategic partnerships, regional trade business prospects through borderless banking, focus on affluent banking, lending in target sectors (oil and gas, infrastructure, agriculture, etc), resumption of oil exports in South Sudan and digital innovation to drive returns. • The asset management product offering is progressing well, hitting an AUM of KES 2.5bn as of December 2024 – three months after launch. • Despite the current headwinds, we foresee continued improvement in interest expenses in the near term in line with CBR rate cuts and easing T-bill rates, which in turn are expected to stimulate credit demand, improve asset quality and lower the cost of funds. | BUY Full Report here |

| Stanchart | • Continued normalisation of revenue earnings in FY25, as signalled by recent MPC rate cuts and consequent easing in the lender’s internal base lending rate, as well as currency stability. • Nonetheless, we view the lender’s cross-border capabilities, diversified investment options, access to capital pools, the drive to provide end-to-end self-service digital options and its global network presence as key tailwinds to the Group’s revenue performance. • The low-cost deposit base and risk-based pricing may help StanChart maintain its net interest margins as the operating environment shifts. • Litigation relating to a longstanding pension issue remains a key overhang, especially given the ruling by the Court of Appeal. Though the case is now at the Supreme Court, contingent liabilities remain a concern due to the potential impact of ongoing court cases in the event of an adverse ruling. • Attractive dividend policy (c. 80% payout), given management’s commitment to grow shareholder return, provided that it meets its capital adequacy requirements. • Improving asset quality to provide opportunities for further reduction in provisions. | BUY Full Report here |

Macro Context

Key indicators suggest a gradual improvement in business environment

Review

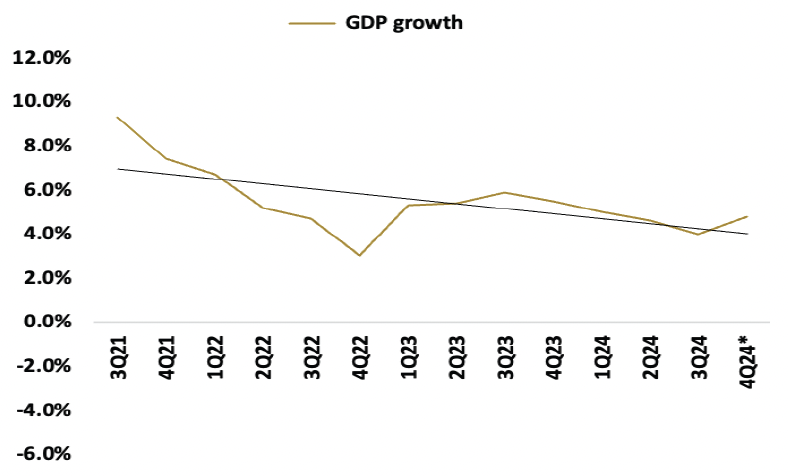

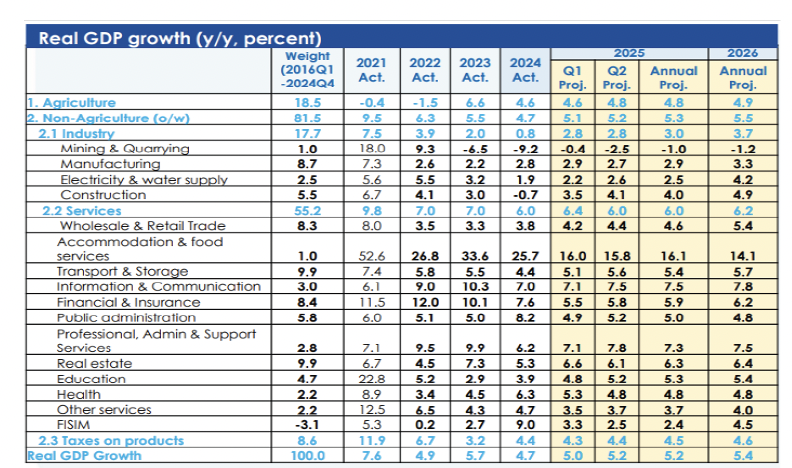

- The performance of the Kenyan economy slowed down in 2024, with GDP growing by 4.7% compared to 5.7% in 2023, pointing to a deceleration in growth in most sectors of the economy (esp. the construction and mining & quarrying sectors).

- The economic slowdown stemmed from multiple challenges, including floods, high interest rates, and subdued business sentiment following protests and reduced development spending.

- Despite resilient agriculture, strong remittance inflows, and a rebound in services, growth was further dampened by weak industrial activity, sluggish private consumption, and policy uncertainty that constrained investment and formal employment growth.

Outlook:

- The projected growth rate of the economy in 2025 has been revised downwards to 5.2% from 5.4%, on account of higher trade tariffs, slower than expected global growth and in turn weaker demand, persistent geopolitical conflicts and their potential impact on supply chains (CBK estimates).

- The World Bank holds a more conservative outlook, with FY25 GDP projected at 4.5%, largely due to tighter global financial conditions, mounting fiscal pressure, and sluggish private sector activity.

- According to CBK, leading indicators of economic activity point to improved performance in the first quarter of 2025. The resilience of key service sectors and agriculture, expected recovery in growth of credit to the private sector, improved exports, stable exchange rates, contained inflation, and improved FX reserves are expected to support economic activity in 2025.

Local unit remains steady against most currencies

- In 1Q25, the shilling exhibited relative stability against most of the currencies we track, with only minor fluctuations. The most notable movement occurred with the TZS, which appreciated earlier in the year due to dollar inflows, but this gain was soon reversed, with KES regaining strength. Specifically, the shilling closed the quarter on a mixed note, depreciating against the JPY, EUR, GBP, and UGX. However, it remained steady against the US dollar and appreciated against the TZS.

- A significant change implemented by the CBK, which we believe plays a crucial role in maintaining the stability of the shilling, was the shift in the reporting system from indicative rates to weighted average rates of registered spot trades in the interbank foreign exchange market. This adjustment means that large trades now have a greater influence on the rate, and as is well known, banks tend to offer more favorable rates for larger transactions.

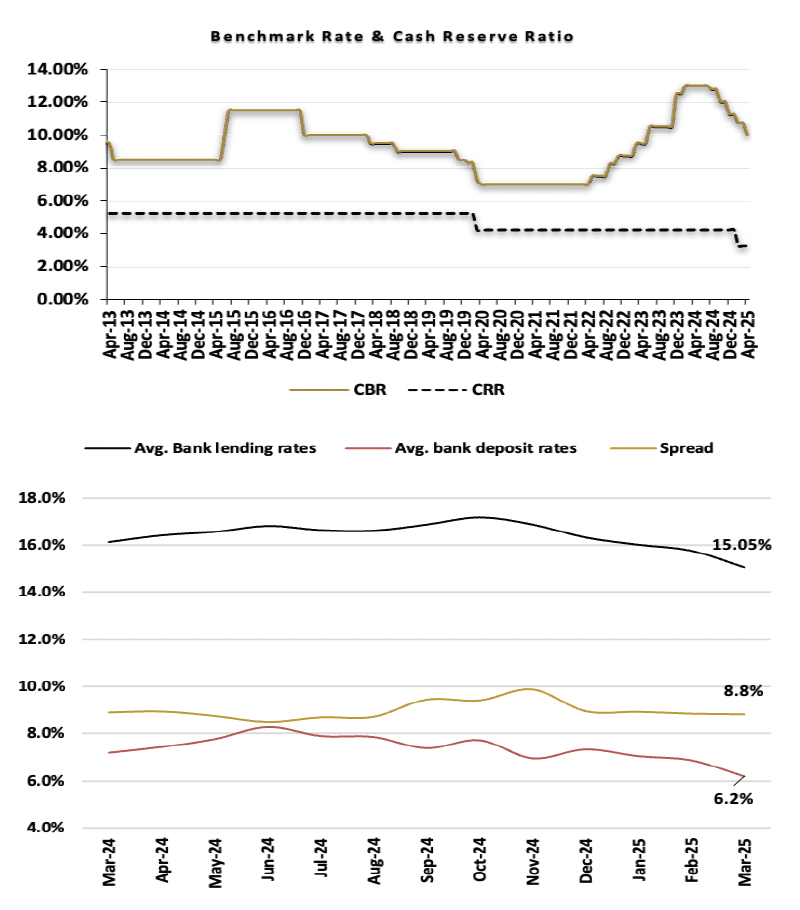

CBK makes bold rate cuts to spur private sector activity

- In 1Q25, the Central Bank’s Monetary Policy Committee (MPC) met once, kicking off the year with a 50bps reduction in the Central Bank Rate (CBR), lowering it from 11.25% to 10.75%.

- The committee also reduced the Cash Reserve Ratio (CRR) to 3.25%, down from 4.25%, a level maintained since March 2020. In a subsequent development, the CBK further lowered the CBR by 75 bps during their second meeting in April, bringing it to 10.0%.

- Inflation closed the quarter at 3.6%, with an average of 3.5%, remaining below the CBK’s mid-point target. Markedly, the NPL ratio increased to 17.2% as of February 2025 (worsened to 17.6% as of April 2025).

- Commercial banks’ lending rates began to decline gradually (average of 15.6% in 1Q25 vs. 15.7% in 1Q24), partly reflecting the reduction in short-term rates and the lower cost of funds.

- Furthermore, savings and term deposit interest rates softened by c. 30bps y/y to an average of 6.7% in 1Q25 vs 7.0% in 1Q24.

- The government’s cost of borrowing continued to fall in the quarter (yields on government securities exhibited a downward trend since October 2024, which we believe is largely influenced by lower benchmark rates and flexibility in bid management).

- By the end of 1Q25, the yield curve had declined by 438.35bps y/y and 133.48bps q/q.

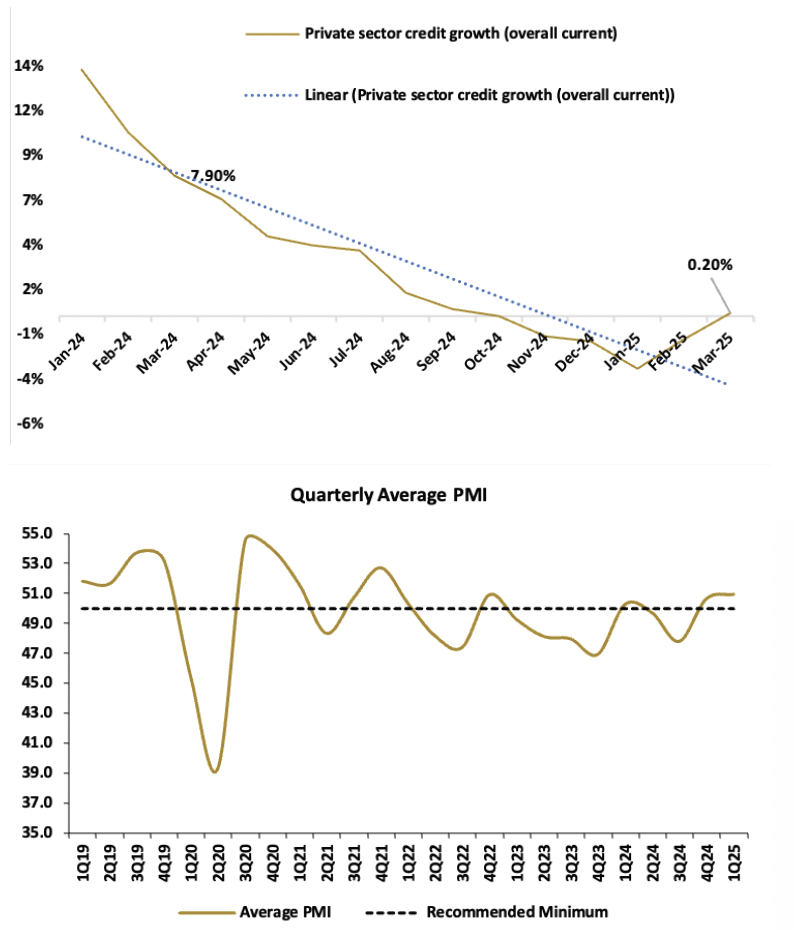

Private sector demand gradually picks up despite a lethargic start to the year

- Private sector credit growth stood at a modest 0.2% in March 2025, with an average contraction of 1.3% in the quarter.

- Drilling down to a sectoral view, manufacturing and construction bore the brunt of reduced credit as lenders mitigate credit risk, with the manufacturing sector experiencing the largest contraction.

- Regarding private sector credit, the impact of a stronger shilling cannot be overlooked. With the stability of the Kenyan shilling, credit growth is now anticipated to be more organic.

- However, caution is warranted, as several headwinds may impede faster credit expansion. These include government borrowing crowding out the private sector, unresolved pending bills, narrower margins, and more cautious lending behaviour by banks.

- Private sector business conditions began the year on a relatively positive note, with the Purchasing Managers’ Index (PMI) averaging 50.9 in 1Q25—slightly above the 50.6 and 50.3 recorded in 4Q24 and 1Q24, respectively.

- Despite the major challenges of input costs, we expect some improvement due to a combination of factors, including lower cost of credit.

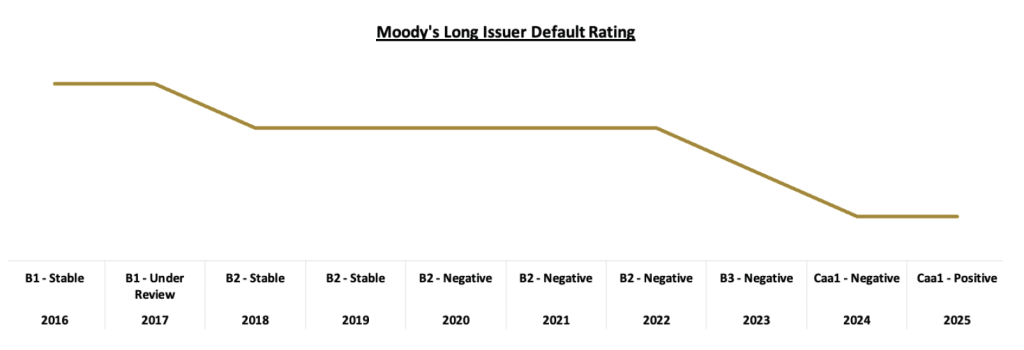

Kenya earns first positive outlook from Moody’s since 2007 in 1Q25

- In 1Q25, Moody’s revised the country’s outlook to positive while maintaining the long-term rating at Caa1. In contrast, Fitch Ratings retained both the B- rating and a stable outlook. The key highlight was Moody’s shift from a negative to a positive outlook, which stood in contrast to the other major rating agencies, all of which revised their outlooks to stable.

- However, the prevailing market conditions at the time—particularly about borrowing costs—may have contributed to their more cautious stance.

- Notably, the positive outlook from Moody’s marked the first time since 2007 that the agency assigned a positive outlook to Kenya. This shift suggests either a recovery from a historically low or unfavourable position, or signals that structural monetary and fiscal adjustments are either anticipated or already underway.

- Looking ahead, a potential upgrade largely hinges on fiscal performance as the country approaches the peak of the budget process and the availability of external funding.