Economic Downshift

A softer jobs report may have shifted rate cut expectations forward. Data during the week showed fewer job openings, lower wages and higher unemployment – with some going as far as calling the week’s jobs report a ‘goldilocks report’. Early as it may be to make goldilocks pronunciations, the hot jobs market may have given its first sign of losing steam, bringing into focus the Fed’s rate cut timeline. CME’s Fed watch tool now shows reviving hopes of a first 25-basis points cut in September, with markets pricing in nearly two cuts within the year.

Data highlights: The Federal Reserve kept interest rates unchanged at 5.50%. U.S. jobs report came in softer than expected: Nonfarm payrolls printed 175k (315k previous, 238k expected), U.S. unemployment increased to 3.9% (3.8% previous and expected), and average hourly earnings increased less than expected at 3.9% y/y in April (4.1% prior, 4.0% expected). German consumer prices increased 2.2% y/y in April, less than the expected 2.3%, while German GDP shrunk 0.2% y/y in quarter 1. Eurozone CPI came in at 2.4% y/y in April. U.S. Consumer confidence dropped to 97.0 (103.1 previous, 104.0 expected), reflecting waning optimism in the economic outlook.

Week ahead: Reserve Bank of Australia Interest Rate Decision – Tuesday | Bank of England Interest Rate Decision, U.S. Initial Jobless Claims – Thursday | U.K. GDP – Friday.

Global Markets Overview

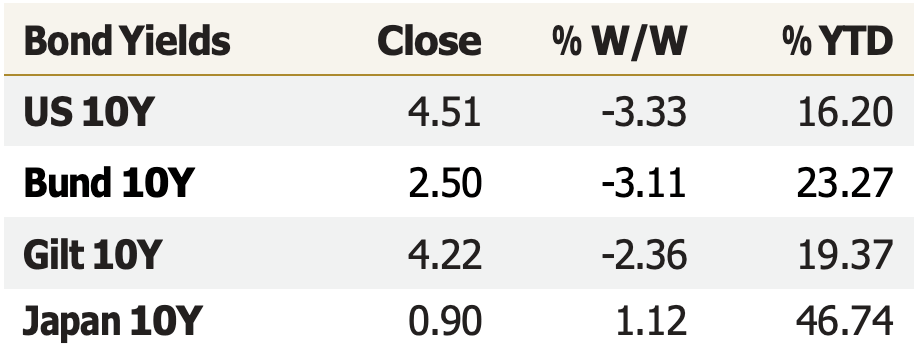

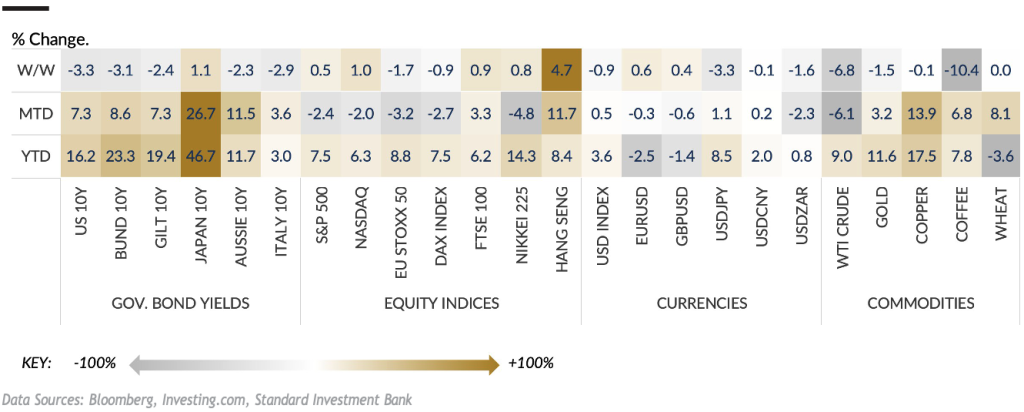

Treasury yields experienced their biggest weekly decline in at least three months as a tepid jobs report raised rate-cut hopes. The yield on the U.S. 2-year treasury fell 19.4 bps during the week – the largest decline since Jan. The yield on the 10- year U.S. treasury dropped 17 bps during the week – the largest weekly drop since December. Fed Chair Powell also rebuffed the possibility of interest rate increases during the week as the Fed held its rates, contributing to treasuries snapping their four-week winning streak. CME data shows reviving expectations of a September 25-bps interest rate cut.

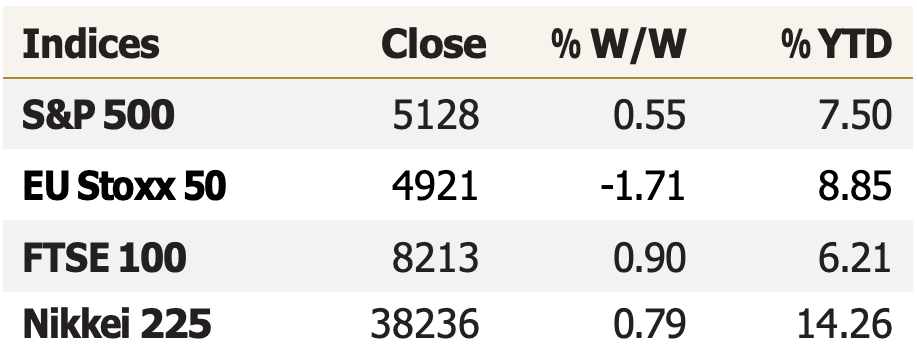

Equities: Last week was the heaviest first quarter earnings week for the companies on Wall Street. 171 earnings released this week contributed 28.50% to S&P 500 Index. Of these companies that reported during the week, 135 beat estimates. This is currently in-line with the trend so far as 79.4% of the 397 companies to have reported beating estimates. The “upside surprise” this quarter for S&P 500 EPS is +8.4% bigger than the three previous quarters, which were quite strong in the mid to high-single digits. This shows that earnings are decent, and it’s more than just the Magnificent 7. Almost every sector of the S&P 500 except industrials and health care are showing higher expected growth rates for ’24 (full year) than at the start of the year. Our stock of the week is Royal Philips NV which soared almost 30% during the course of the week as the Dutch health-technology group announced it would pay a much lower-than-expected $1.1 billion settlement to resolve personal injury and medical monitoring litigation in the U.S. The settlement is far below the $4 billion some had expected, with worst-case fears reaching $10 billion that had weighed down on the stock over the last couple of years.

Currencies: The Japanese Yen was king of currencies for the week – registering its largest weekly gain in seventeen months against all its major counterparts as the market suspected a Bank of Japan intervention. The U.S. Dollar retreated – losing 3.33% against the Japanese Yen, for its largest one-week percentage decline since December 2022. The Dollar index snapped a three-week winning streak as the greenback lost against its major peers following soft labour data. The Euro climbed to an over three-week high, the Australian Dollar hit three-and-a-half-month highs, the Sterling Pound jumped to three-week highs and the Canadian Dollar hit four- week highs.

Commodities: Crude oil prices dropped to one-and-a-half-month lows on easing geopolitical tensions. Natural Gas snapped a three-week losing streak, soaring 32.7% during the week to a 13-week high on emerging supply concerns. Cocoa fell 24% during the week as funds liquidated long positions sparked partly by rising margin calls. Coffee retreated from the previous week’s record high, dropping 12.9% as traders liquidated long positions. Sugar was slightly lower, supported by concerns that hot weather in Thailand could damage sugarcane crops.

Performance of Major Global Financial Assets

Disclosure and Disclaimer

Analyst Certification Disclosure: The research analyst or analysts responsible for the content of this research report certify that: (1) the views expressed and attributed to the research analyst or analysts in the research report accurately reflect their personal opinion(s) about the subject securities and issuers and/or other subject matter as appropriate; and, (2) no part of his or her compensation was, is or will be directly or indirectly related to the specific recommendations or views contained in this research report.

Global Disclaimer: Standard Investment Bank (SIB) and/or its affiliates makes no representation or warranty of any kind, express, implied or statutory regarding this document or any information contained or referred to in the document. The information in this document is provided for information purposes only. It does not constitute any offer, recommendation or solicitation to any person to enter into any transaction or adopt any hedging, trading or investment strategy, nor does it constitute any prediction of likely future movements in rates or prices, or represent that any such future movements will not exceed those shown in any illustration. Past performance is not indicative of comparable future results and no representa- tion or warranty is made regarding future performance. While we endeavour to update on a reasonable basis the informa- tion and opinions contained herein, there may be regulatory, compliance or other reasons that prevent us from doing so. Accordingly, information may be available to us which is not reflected in this material, and we may have acted upon or used the information prior to or immediately following its publication.