Harnessing momentum to grow value: Listing planned in 2026

Executive Summary

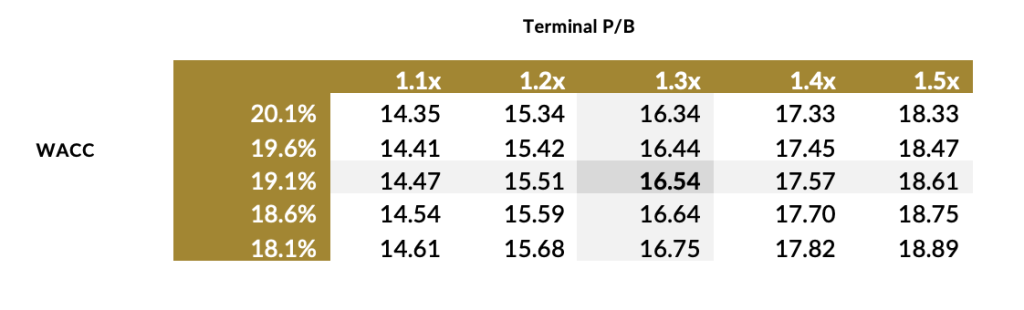

We initiate coverage on Family Bank Group, with the fair value estimate of KES 16.54. In 1Q25, the bank posted a +15.4% y/y PAT increase, supported by a 32.4%y/y jump in operating income, with loans up by 10.1% y/y – a commendable performance compared to peers in 2025. While the cost-to-income ratio is higher than the industry at over 60%, we believe it also provides scope for improvements with new products and an extended branch network, which is increasingly providing the necessary scale. The bank has also started tapping into Development Finance Institutions (DFI) funding; two notable ones in 2025 being €50m from European Investment Bank development arm European Global and $20m from British International Investment (BII) to finance SME’s, women-led firms and agribusinesses. We believe the bank is also at the cusp of moving from a Tier 2 Bank to a Tier 1.

Positioning itself strategically as the preferred bank for business. Established over 40 years ago as Family Bank Building Society by Titus Muya, Family Bank has emerged as a mass market entity across Kenya, positioning itself as the preferred bank for biashara ‘business’ – the bank to go for every business person, regardless of the size. In 2024, the bank won the best Tier 2 Bank for excellence in banking customer experience by the Kenya Bankers Association.

Planned Listing and Capital Market Access. The Group’s plan to list on the Nairobi Securities Exchange in 2026—through either introduction or IPO—aims to unlock share liquidity (having traded in the OTC market since 2006) and potentially raise new capital, considering the robust growth (+31.4 % y/y CAGR from FY20 to FY24). The moderate decline in capital adequacy ratios since FY21 (15.8% in 1Q25) alongside the maturity of its KES 4.0bn medium-term note on 17th December 2026 frames an opportune moment. A recovering capital market is anticipated to provide a conducive environment, with the listing expected to enhance liquidity, capital appreciation potential, and a dilution pathway for investors seeking to comply with the Central Bank of Kenya’s maximum shareholding requirements.

Key Risks to Our Thesis. Family Bank has a high cost-to-equity ratio at over 60%, which isn’t unusual for Tier 2 Banks, and which we expect shall improve as the bank continues to achieve scale. The market it serves has proved problematic for other banks in the past, including managing NPLs and migration of customers to other banks when the SME’s scale, which may prove to be the ‘Achilles’ heel. Governance remains an important element to consider, but this has improved considerably over the years. As a committed dividend-paying bank, we think the fast growth could limit the payout levels over the years. Management has guided a dividend policy of not less than 30.0%.

Investment Summary & Valuation. We estimate the fair value estimate for Family Bank at KES 16.54. By a terminal price to book (P/B) ratio of 1.26x (based on the average P/B of recent precedent transactions), we estimated the terminal value of the business beyond the 2029 forecasted period at KES 48.3bn. The cost of equity used in discounting the cash flows is derived by building up the value on a theoretical basis to arrive at a rate of 21.9%. On a 75%/25% weighting for debt and equity, respectively, we estimated the Weighted Average Cost of Capital (WACC) at 19.1%, with the cost of debt of 10.6%, derived from the weighted interest on Family Bank’s debt. We used the price-to-book value summary table below: