Highlights

Stock markets kicked off the week sharply lower after President Trump, in his usual unexpectedly expected fashion, stated that the U.S. would be implementing 25% tariffs on imports from the neighbouring Mexico and Canada, along with a 10% tariff on imports from China. However, the tariffs on Mexico and Canada were postponed by the end of day Monday, to allow for further negotiations between the involved nations in an attempt to strike a longer-lasting deal. This pause, along with robust earnings growth by U.S. companies helped the stocks recover some of their early losses by week’s end.

Data highlights:

The February Jobs data showed that the U.S added 143K jobs, slightly lower than the analyst expectations of 173K jobs. Unemployment rate declined to 4.0% (4.1% previous, 4.1% expected). Initial jobless claims also ticked higher, coming in at 219K from 208K previously and against the analyst consensus figure of 213K. Further, job openings came in at 7.60Mn, down from the upwardly revised 8.156Mn in the previous month and below the expected 8.00Mn openings. Over in Europe, the Eurozone inflation rate ticked up by a tenth of a percent to 2.5% (2.4% expected) while retail sales grew at 1.9% in line with analysts’ expectations. In the U.K, the Bank of England cut its benchmark interest rate by a quarter a percent to 4.5%, in line with analysts’ consensus.

Week ahead:

U.S. CPI– Wednesday | U.K. GDP, U.S. PPI – Thursday | Eurozone GDP & Employment change, U.S. Retail Sales – Friday.

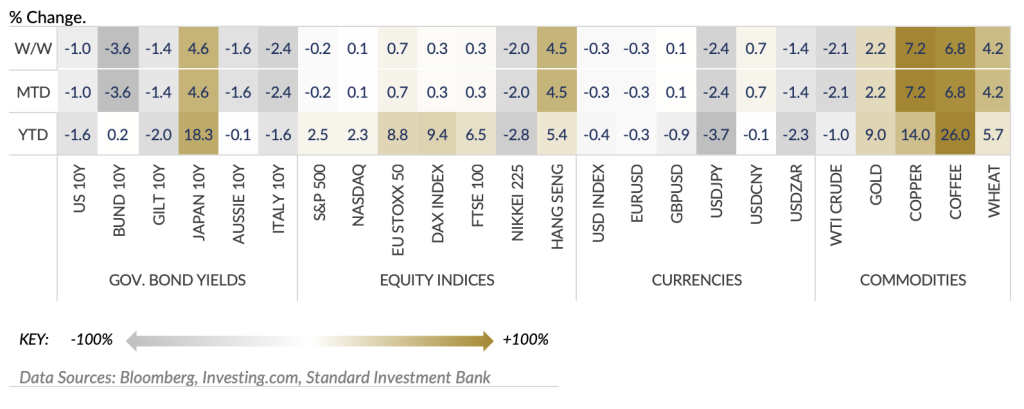

Global Markets Overview

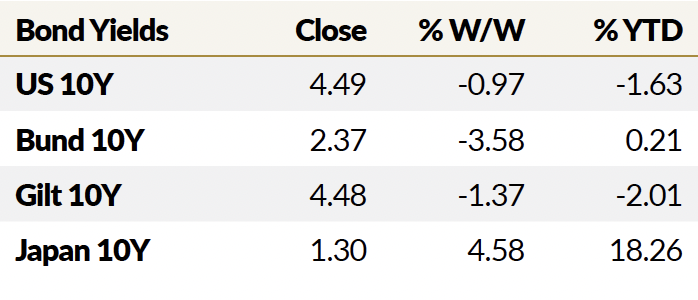

Treasury yields

U.S. Bond Yields ticked higher for the two-year and five-year treasuries while the ten-year yields traded lower for a fourth consecutive week as investors priced in the near-term inflationary risks associated with the tariffs imposed by the U.S. president. The U.S. yield curve flattened in the week with the spread between the two- and ten-year yields narrowing to 21 basis points from 34 basis points the week before. Yields in Europe were lower across the German curve, with the spread remaining largely the same week on week at 33 basis points. Yields in Japanese bonds rose for a fifth-consecutive week following hawkish remarks from the Bank of Japan bolstered expectations of further interest rate hikes within the year.

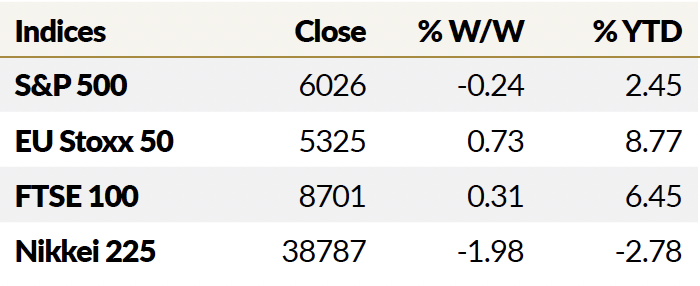

Equities:

The S&P 500 Index and the Dow Jones Industrial Average ended the week marginally lower with significant volatility being witnessed in a week packed with market moving headlines. The tech heavy Nasdaq eked out a small gain of just under a tenth of a percent. In Europe, stocks traded largely higher as illustrated by the EU 50 and German DAX indices. Japanese stocks tumbled over 1.5% as traders rushed to safety following increased expectations of interest rate hikes by the apex bank. Uber Technologies Inc rallied over 11% making it our stock of the week following its latest earnings report as revenues and gross bookings topped estimates. On the company’s earnings call, CEO Dara Khosrowshahi acknowledged that although the company continues to deliver solid growth and margin expansion, there remains a currency risk especially for operations in Argentina, Mexico, and Brazil, three of the top 20 countries Uber operates in. But while the company will feel its impact on the top-line, the bottom-line is insulated from currency fluctuations as drivers and merchants are paid in local currencies, creating a natural hedge. The CEO confirmed the company’s commitment to Autonomous Vehicles and its place as the indispensable go-to-market partner for Autonomous players with aggressive investment. This led to many analysts maintaining a Buy rating with majority of them raising price targets. This view was affirmed on Friday as Bill Ackman declared “We believe that Uber is one of the best managed and highest quality businesses in the world.”

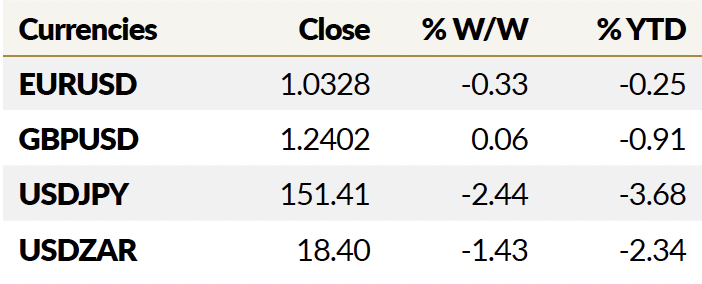

Currencies:

The U.S. Dollar shed its value against a majority of the major currencies except the Euro. Significant losses were witnessed against the Japanese Yen as the Asian currency rallied just under 2.5% against the Dollar following hawkish remarks by the Bank of Japan on the upward path of its interest rates. The Canadian Dollar also staged a remarkable rally, gaining about 1.7% against its neighbour, following the prompt withdrawal of tariffs announced by the U.S. President. Traders were of the opinion that the postponement of the tariffs backed the hypothesis that President Trump would not follow through with the tariff threats but rather he would use them as a bargaining tool for more favourable trade agreements from a U.S. perspective.

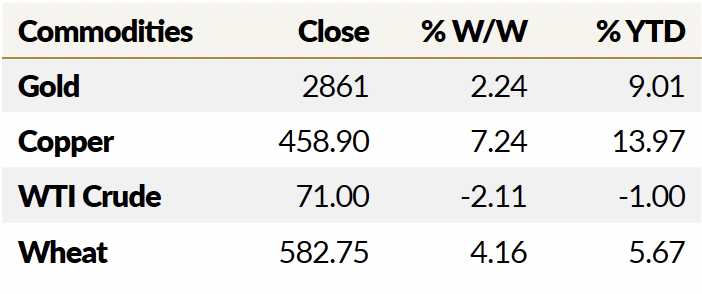

Commodities:

Silver, Gold and Copper shone through the week gaining 1.63%, 2.24% and 7.24% respectively. Natural Gas gained a whopping 8.71% for the week, after China announced retaliatory tariffs of 15% on its Natural Gas exports to the U.S. Oil shed 2.11% capping a third consecutive week of price declines. Agricultural commodities Wheat, Corn, Sugar and Coffee also gained, closing the week 4.16%, 1.14%, 0.72% and 7.01% percent higher. On the other hand, Cocoa prices declined for a second week in a row, shedding 8.82%, due to slowing demand for the commodity as the high prices for the product force chocolate makers to reformulate recipes by replacing cocoa with other ingredients.

Performance of Major Global Financial Assets