Review of banking sector multiples: The sector is still undervalued

Definitions:

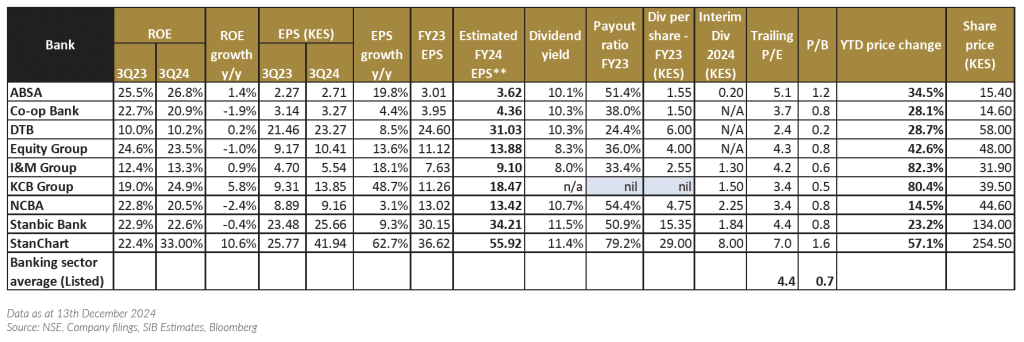

ROE: Measures how efficiently a company is generating income from the equity investments of its shareholders; >10% is considered healthy; the higher the better;

EPS: Measure of a company’s profitability that indicates how much profit each outstanding share of common stock has earned; the higher the better.

Dividend yield: Represents the dividend amount a company pays annually compared to its share price.

Payout ratio: Calculated by dividing the total dividends by the total net income of a company.

P/E: The price an investor is willing to pay for each shilling of a company’s earnings – If below average, considered undervalued.

P/B: Calculated by dividing a company’s market price by its book value of equity (shareholder’s equity per share). A ratio below one indicates that a company is undervalued, while a ratio above one indicates that the company’s stock is trading at a premium.

Stock Recommendations

Absa

- We note the slowdown in earnings growth in the year, largely due to rising provisions and growing interest expenses.

- Overall, we see the lender’s growth in customer base, subsidiaries’ value proposition, increase in service touchpoints, product diversification, and strategic partnerships as revenue drivers in the long term.

- Despite a slight uptick q/q, Absa’s CTI ratio remains below the 40% mark, thereby providing it with headroom to continue its digital investment initiatives, further supported by its robust capital levels.

- Tech adoption and automation are expected to smoothen costs in the long run while increasing efficiency.

- Decline in asset quality is a concern though it is still below the industry average.

- With the rise in NPLs, we opine the lender will focus more on short-term working capital lending, secured loans (affordable housing, asset finance) and target payrolls that pass through the bank.

- Intention to go big on retail segment to boost growth though may see cost of risk rise.

- Recommendation: BUY

Co-op Bank

- The lender’s strong franchise base, diversified revenue streams, focus on digitization and value proposition for its core customers, SACCOs, are expected to drive the Group’s revenue in the long term.

- The addition of the counter to the MSCI Frontier Markets index is anticipated to prop up valuation from a price perspective given anticipated foreign investor visibility.

- Strong capital and liquidity base to offer headroom to lend.

- Strategic partnerships with access to funding for onward lending to MSMEs.

- Cautious repricing of loan portfolio to help balance NPL management and revenue generation. Continued rise in FX income on attractive spreads.

- NPL however ticked upwards in the period, leading to a rise in loan loss provisioning.

- Recommendation: BUY

Diamond Trust Bank

- The lender’s growth initiatives, recent corporate reorganization, diversified revenue lines (custody business, agency banking), ecosystem focus, strategic partnerships and regional reach as tailwinds to the Group’s long-term outlook.

- Notably, interest expense may continue to weigh on the Group’s topline in the near term. The lender plans to grow its customer base to 10m in East Africa by 2026 –an ambitious feat.

- Group costs are poised to remain elevated as it continues to expand, enhance digital capabilities and recruit more staff to deliver its business growth strategy.

- Potential increase in loan provisions in 4Q24 as asset quality deteriorates.

- Trading at a significant discount to its book value; entry point for investors with a long-term play.

- DTB’s addition to the MSCI Frontier Markets Small Cap index is anticipated to prop up valuation from a price discovery perspective given added investor visibility.

- Recommendation: BUY

Equity Group

- Equity Bank Kenya’s performance remains tepid. Receipt of principal approval for its health insurance offering and approval for its general insurance offering provides an opportunity to grow NFI.

- The group is looking at refreshing its investment bank’s strategy and developing enhanced products in 2025 as it looks to potentially tap into the asset management space.

- Decline in loan yields may cause some pressure on margins however it may help stem NPLs and stimulate credit demand.

- Restructuring of the Group balance sheet from repayment of borrowings to contain interest costs.

- Loan loss provisions are however robust and provide a potential write-back opportunity once NPLs decline.

- Recommendation: BUY

I&M Group

- Continued growth in Personal and Business Banking business on the back of enhanced propositions; unsecured digital lending, stock financing, digital self-onboarding etc.

- Proposed foray into agency banking, entry into oil & gas, leasing and public sectors, ecosystems play, the launch of a China desk and expansion of its wealth management & advisory portfolio are forecasted to act as tailwinds to boost transactions as well as non-funded income.

- Continued implementation of the risk-based model should help the lender grow its net interest income as customer numbers increase.

- The recently proposed subscription offer to issue 86.5m new shares to East Africa Growth Holding at KES 48.42 is anticipated to pump in additional capital (approx. KES 4.2bn) to further support the lender’s iMara 3.0 growth strategy

- Recommendation: BUY

KCB Group

- KCB Group is on track for strong performance in EPS in FY24, given the lender’s sustained revenue growth (has already surpassed its FY23 earnings by KES 14.6bn in 3Q24).

- Deepening digital capabilities to support growth in NFI and operational efficiencies.

- Growing subsidiary contribution to PAT & assets and the continued recovery of KCB Kenya. NPLs will remain elevated in the near term given macro conditions in Kenya.

- However, the slowdown in Gross NPL increase from the preceding quarter could point to a peak in NPLs. Potential writebacks on potential asset recovery mechanisms as well as the reduction in interest rates as signaled by MPC rate cuts (both locally and internationally).

- Sale of NBK (which is awaiting regulatory approval from the CBK), capital buffers as well as the stellar performance recorded in the preceding quarters, are anticipated to provide management with an incentive to pay an attractive final dividend in FY24.

- Recommendation: BUY

NCBA

- The lender’s results point to a moderated growth for the remainder of the year.

- Product and channel diversification, as well as regional markets, should secure solid profitability in the long term (subsidiaries contributed 13% of group PBT in 3Q24).

- Costs are however expected to remain elevated in the short term given the ongoing digital and physical expansion initiatives.

- The acquisition of AIG insurance, digital offering, and robust wealth management business to drive NFI.

- Cost of funds may squeeze interest margins on higher interest expense on deposits.

- Recommendation: BUY

Stanbic Bank

- Coming from a high base in 2023, we do not see a significant shift in revenue performance in FY24.

- Growth in its Asset Management and Insurance Business to grow non-interest revenue as the bank positions itself to tap into its Personal & Private Banking segment.

- Growth opportunities exist in the medium term from regional trade business prospects through borderless banking, growing lending in target sectors (oil and gas, infrastructure, agriculture etc), and digital innovation to drive operational and cost excellence.

- Recent CBR rate cuts to help address customer deposit expenses. FX trading income is anticipated to remain muted in the year.

- Recommendation: BUY

Stanchart

- Robust interest margins on higher interest income, with a high CASA rate (97% as of FY23) anticipated to help manage the cost of funds.

- Digitization of services will see higher onboarding of both retail and business clients and increased uptake of loans and diversified wealth management solutions and drive NFI.

- Attractive dividend policy (c. 80% payout) – interim dividend up 33.3%y/y to KES 8.00.

- Asset management growth is steady, with SC Shilingi up to KES 10.0bn as of July 2024, and the lender’s key Affluent segment’s AUM hitting KES 185.5bn as of FY23.

- Cost efficiencies to support the lender’s bottom line. Improving asset quality to provide opportunities for reduction in provisions in 4Q24.

- Recommendation: BUY