Resilience Amidst Shifting Tides

Investment Thesis Summary

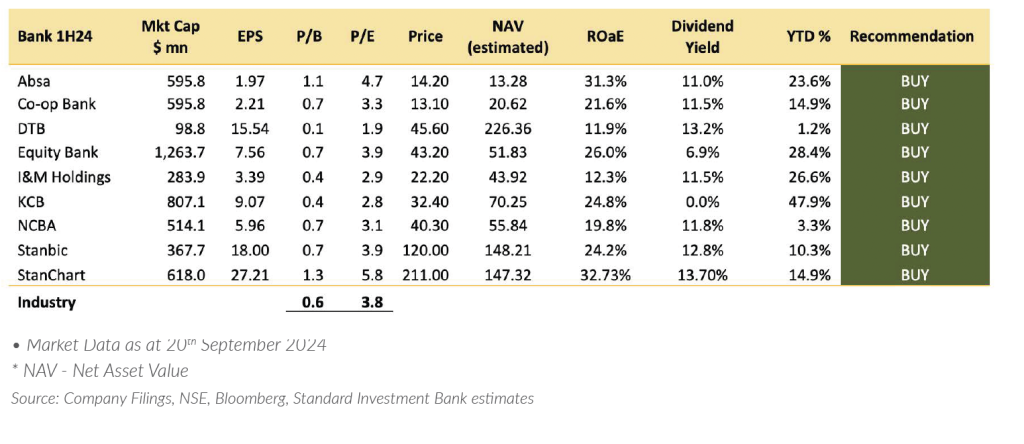

The banking sector has exhibited remarkable resilience in the face of challenging macroeconomic conditions, with lenders in our coverage reporting profit growth (at varying intensities) in the face of a persistently high-interest rate regime which has not only raised the cost of funds but also raised overall asset quality deterioration; major climate event – floods. We believe the lenders’ ability to balance credit risk management with revenue growth as well as healthy capital buffers buoyed performance in the face of sluggish credit demand. We are optimistic about the performance of the sector in the second half of 2024. We view ongoing revenue diversification strategies, continued implementation of risk-based pricing, support from regional subsidiaries, regional trade deals, cost containment initiatives, and digital transformation as tailwinds to the sector. Additionally, potential rate cuts (both internationally and locally) as inflation eases are expected to stimulate private-sector credit demand, reducing the crowding-out effect.

We believe banking stocks present attractive capital appreciation – given that most listed banks are trading at below book value and still have healthy income opportunities and growth – especially as signalled by interim dividend increase by StanChart and Stanbic and the resumption of dividend payment by KCB Group. The addition of DTB to the MSCI Frontier Markets Small Cap index, as well as the addition of Cooperative Bank of Kenya to the MSCI Frontier Markets index and the recent Fed 50 bps rate cut, will provide stock visibility and reorient foreign investor interest into frontier and emerging markets.

Key risks to our investment thesis include the adverse effects of a higher for longer interest rate environment squeezing margins, potential impact of credit agency ratings on the cost of credit, cybersecurity threats, escalating geopolitical tensions, sovereign debt risks, supply chain disruptions, slower than expected economic growth, elevated NPL stock, uncertain tax regime and increased regulatory pressure.